BLOG

In Certain Situations, Filing a Gift Tax Return is Required or Recommended

Thanks to the annual gift tax exclusion, you can systematically reduce your taxable estate with little effort. And while you typically don’t have to file a gift tax return, in some situations, doing so may be required or recommended.

Know when a return is required

The annual gift tax exclusion amount for 2024 is $18,000 per recipient. (It’ll increase to $19,000 per recipient beginning in 2025.)

So, for example, if you have three children and seven grandchildren, you can give up to $180,000 in 2024 ($18,000 x 10) without gift tax liability. Under this scenario, you aren’t required to file a gift tax return.

If your spouse consents to a “split gift,” you can jointly give up to $36,000 per recipient in 2024. When making split gifts, you must file a gift tax return (unless you reside in a community property state). If your gift exceeds the annual gift tax exclusion amount, the federal gift and estate tax exemption may shelter the excess from tax if a gift tax return is filed. In 2024, the exemption amount is an inflation-adjusted $13.61 million. In 2025, the exemption amount increases to an inflation-adjusted $13.99 million.

Avoid a filing penalty

Failing to file a required gift tax return may result in a penalty of 5% per month of the tax due, up to 25%. Bear in mind that you might file a gift tax return even if you’re technically not required to do so. The return establishes the value of assets for tax purposes and provides a measure of audit protection from the IRS.

If you file a gift tax return and honestly disclose the value of the gifts, a safe-harbor rule prohibits audits after three years. However, the safe-harbor rule doesn’t apply in the event of fraudulent statements or inadequate disclosure.

Mind the filing deadline

The due date for filing a gift tax return for 2024 is April 15, 2025, the same due date for filing an individual income tax return. If you file for an extension, the filing due date is October 15, 2025. Contact FMD if you have questions about whether a gift requires filing a gift tax return.

Sharing Your Estate Plan’s Details with Family has Pros and Cons

When it comes to estate planning, one important decision many people struggle with is whether to share the details of their plans with family members. There’s no one-size-fits-all answer — it largely depends on your goals and your family’s dynamics. However, thoughtful communication can go a long way in reducing confusion and conflict after your death. Let’s take a closer look at the pros and cons of sharing your estate planning decisions with your family.

The pros

Sharing the details of your estate plan provides many benefits, including:

Explaining your wishes. When they design their estate plans, most people want to treat all their loved ones fairly. But “fair” doesn’t always mean “equal.” The problem is that your beneficiaries may not understand that without an explanation.

For example, suppose you have adult children from a previous marriage and minor children from your second marriage. Treating both sets of children equally may not be fair, especially if the adult children are financially independent and the younger children still face significant living and educational expenses. It may make sense to leave more of your wealth to your younger children. And explaining your reasoning upfront can go a long way toward avoiding hurt feelings or disputes.

Obtaining feedback. Sharing your plans with loved ones allows them to ask questions and provide feedback. If family members feel they’re being treated unfairly, you may wish to discuss alternatives that better meet their needs while still satisfying your estate planning objectives.

Streamlining estate administration. Sharing details of your plan with your executor, trustees and any holders of powers of attorney will enable them to act quickly and efficiently when the time comes. This is particularly important for people you’ve designated to make health care decisions or handle your financial affairs if you become incapacitated.

The cons

There may be some disadvantages to sharing the details of your plan, including:

Strained relationships. Some loved ones may be disappointed when they learn the details of your estate plan, which can lead to strained relationships. Keeping your plans to yourself allows you to avoid these uncomfortable situations. On the other hand, it also deprives you of an opportunity to resolve such conflicts during your lifetime.

Encouragement of irresponsible behavior. Some affluent parents worry that the promise of financial independence may give their children a disincentive to behave in a financially responsible manner. They may not pursue higher education, remain gainfully employed and generally lead productive lives. Rather than keeping your children’s inheritance a secret, a better approach may be to use your estate plan to encourage desirable behavior.

Don’t forget to factor in your state’s laws

As you think over how much you wish to disclose to your loved ones about your estate plan, be sure to consider applicable state law. The rules governing what a trustee must disclose to beneficiaries about the terms of the trust vary from state to state. Some states permit so-called “quiet trusts,” also known as “silent trusts,” which make it possible to keep the trust a secret from your loved ones.

Other states require trustees to inform the beneficiaries about the trust’s existence and terms, often when they reach a certain age. For example, trustees may be required to provide beneficiaries with a copy of the trust and an annual accounting of its assets and financial activities. However, many states allow you to place limits on the information provided to beneficiaries.

Sharing is caring

Ultimately, a well-crafted estate plan should speak for itself. But open communication, when done thoughtfully, can support your plan’s success and give your loved ones clarity and peace of mind. Contact FMD with questions.

If Your Estate Includes IP, Consider these Planning Strategies

Over your lifetime, you’ve likely accumulated various tangible assets. These may include automobiles, personal property or art. It’s relatively easy to account for such assets in your estate plan, but what about intangible assets, such as intellectual property (IP)? These assets behave differently from other types of property, so careful planning is required to preserve their value for your family.

What is IP?

IP generally falls into one of four categories: patents, copyrights, trademarks and trade secrets. Let’s focus on only patents and copyrights, creatures of federal law intended to promote scientific and creative endeavors by providing inventors and artists with exclusive rights to benefit economically from their work for a certain period.

In a nutshell, patents protect inventions. To obtain patent protection, inventions must be novel, “nonobvious” and useful. The two most common patent types are utility and design patents:

A utility patent may be granted to someone who “invents or discovers any new and useful process, machine, manufacture or composition of matter, or any new useful improvement thereof.”

A design patent is available for a “new, original and ornamental design for an article of manufacture.”

Under current law, a utility patent protects an invention for 20 years from the patent application filing date. A design patent lasts 15 years from the patent issue date. For utility patents, it typically takes at least a year to a year and a half from the date of filing to the date of issue.

When it comes to copyrights, they protect the original expression of ideas that are fixed in a “tangible medium of expression,” typically in the form of written works, music, paintings, sculptures, photographs, sound recordings, films, computer software, architectural works and other creations. Unlike patents, which the U.S. Patent and Trademark Office must approve, copyright protection kicks in as soon as a work is fixed in a tangible medium.

For works created in 1978 or later, an author-owned copyright lasts for the author’s lifetime plus 70 years. A “work-for-hire” copyright expires 95 years after the first publication date or 120 years after the date the work is created, whichever is earlier. More complex rules apply to works created before 1978.

What are the estate planning considerations?

For estate planning purposes, IP raises two important questions:

What’s the IP worth?

How should it be transferred?

Valuing IP is a complex process. So it’s best to obtain an appraisal from a professional with experience valuing this commodity.

After you know the IP’s value, it’s time to decide whether to transfer it to family members, colleagues, charities or others through lifetime gifts or bequests after your death. The gift and estate tax consequences will likely affect your decision. However, you also should consider your income needs and who’s in the best position to monitor your IP rights and take advantage of their benefits.

For example, if you continue to depend on the IP for your livelihood, hold on to it until you’re ready to retire or no longer need the income. You also might want to sell or retain ownership of the IP if your children or other transferees lack the desire or wherewithal to take advantage of its economic potential and monitor and protect it against infringers.

Whichever strategy you choose, it’s important to plan the transaction carefully to ensure your objectives are achieved. There’s a common misconception that when you transfer ownership of the tangible medium on which IP is recorded you also transfer the IP rights. IP rights are separate from the work and are retained by the creator — even if the work is sold or given away.

Turn to a professional

Having your assets distributed according to your wishes after your death is a primary reason for having an estate plan. And whether artistic or scientific endeavors are the source of your wealth or simply meaningful diversions, it’s likely that you care deeply about who ultimately possesses your works and enjoys their benefits. Contact FMD to help ensure your estate plan correctly accounts for your IP.

Is Your Business on Top of its Tech Stack?

Like many business owners, you’ve probably received a lot of technology advice. One term you may hear frequently is “tech stack.” Information technology (IT) folks love to throw this one around while sharing their bits and bytes of digital wisdom.

Well, they’re not wrong about its importance. Your tech stack is crucial to maintaining smooth operations, but it can be a major drain on cash flow if not managed carefully.

Everything you use

For the purpose of running a business, a tech stack can be defined as all the software and other digital tools used to support the company’s operations and IT infrastructure. It includes assets such as your:

Accounting software,

Customer relationship management platform,

Project management tools,

Cloud storage, and

Communication apps.

Note: In a purely IT context, the term is widely defined as the set of technologies used to develop an application or website.

For businesses, a tech stack’s objective is to streamline workflows and promote productivity while maintaining strong cybersecurity. Unfortunately, as it grows, a tech stack can leave companies struggling with overspending, inefficiencies and employee apathy.

Case in point: For its 2025 State of Digital Adoption Report, software platform provider WalkMe surveyed nearly 4,000 enterprise leaders and employees worldwide. The data showed that about 43% of enterprise tech stacks are currently more complex than they were three years ago. Disturbingly, the report found the average large enterprise lost $104 million in 2024 because of underused technology, fragmented IT strategy and low employee adoption of tech tools.

Although these results focus on larger companies, small to midsize businesses face the same risks. Over time, companies often layer technologies upon technologies, sometimes introducing redundant or extraneous tools that are largely ignored.

5 factors to consider

Balancing functionality and innovation without overspending is the key to staying on top of your tech stack. Here are five factors to focus on:

1. Composition. Many business owners lose track of the many complex elements of their tech stacks. The best way to stay informed is to conduct regular IT audits. These are formal, systematic reviews of your IT infrastructure, which includes your tech stack. Audits often reveal redundant software subscriptions and underused or forgotten software licenses.

2. Integration/compatibility. When tech tools don’t play well together — or at all — data silos spring up and redundant work drags everyone down. This leads to more errors and less productivity. When managing your tech stack, choose solutions that integrate well across your operations. As feasible, replace those that don’t.

3. Price to value. Choosing IT tools primarily based on cost is risky. Although you should budget carefully, opting for cheaper solutions can ultimately increase technology expenses because of greater inefficiencies and the constant need to add tools to fill functionality gaps. Stay mindful of getting good value for the price and make choices that align with your strategic objectives.

4. Scalability. Generally, as a business grows, its technology needs expand and evolve. That doesn’t mean you always have to buy new software, however. Look for solutions that can scale up with growth or down during slower periods. Shop for assets that offer flexibility along with the right functionality.

5. Adoptability. Your company could have the most powerful software tool in existence, but if it sits unused, that item is just a wasted expense taking up space in your tech stack. Add new technology cautiously. Consult your leadership team, survey the employees who’ll be using it and ask for vendor references. When you do buy something, roll it out with an effective communication strategy and thorough training.

A technological tree

Like a tree, a tech stack can grow out of control and become a nuisance or even a danger to everyone around it. Properly pruned and otherwise well-maintained, however, it can be a powerful and functional business feature. Let FMD help you identify all your technology costs and assess the return on investment of every component of your tech stack.

How Companies Can Better Control IT Costs

Most small to midsize businesses today are constantly under pressure to upgrade their information technology (IT). Whether it’s new software, a better way to use the cloud or a means to strengthen cybersecurity, there’s always something to spend more money on.

If your company keeps blowing its IT budget, rest assured — you’re not alone. The good news is that you and your leadership team may be able to control these costs better through various proactive measures.

Set a philosophy and exercise governance

Assuming your company hasn’t already, establish a coherent IT philosophy. Depending on its industry and mission, your business may need to spend relatively aggressively on technology to keep up with competitors. Or maybe it doesn’t. You could decide to follow a more cautious spending approach until these costs are under control.

Once you’ve set your philosophy, develop clear IT governance policies and procedures for purchases, upgrades and usage. These should, for example, mandate and establish approval workflows and budgetary oversight. You want to ensure that every dollar spent aligns with current strategic objectives and will likely result in a positive return on investment (ROI).

Beware of shiny new toys! Many businesses exceed their IT budgets when one or two decision-makers can’t control their enthusiasm for the latest and greatest solutions. Grant final approval for major purchases, or even a series of minor ones, only after carefully analyzing the technology you have in place and identifying legitimate gaps or shortcomings.

Also, remember that overspending on technology is often driven by undertrained employees. Teach and remind your users to adhere to your IT policies and follow procedures. Doing so can help prevent costly operational mistakes and cybersecurity breaches.

Conduct regular audits

You can’t control costs in any business area unless you know precisely what they are. To get the information you need, regularly conduct IT audits. These are formal, systematic reviews of your IT infrastructure, policies, procedures and usage. IT audits often reveal budget drainers such as:

Redundant subscriptions for software or other tech services,

Underused or forgotten software licenses, and

Outdated or abandoned hardware.

You may discover, for instance, that you’re paying for several different software products with overlapping functionalities. Choosing one and discarding the others could generate substantial savings.

As you search for overspending, also look for examples of IT expenditures delivering a good ROI. You want to be able to refine and repeat whatever decision-making process led you to those wins.

Keep an eye on the cloud

One specific type of IT expense that plagues many businesses relates to cloud services. Like many companies, yours probably uses a “pay as you go” subscription model that includes discounts or rate reductions for lower usage. However, if you don’t monitor your actual cloud usage and claim those discounts or cheaper rates, you can wind up overpaying for months or even years without realizing it.

To avoid this sad fate, ensure that at least one person within your business is well-acquainted with your cloud services contract. Assign this individual (usually a technology executive) the responsibility of making sure the company claims all discounts or rate adjustments it’s entitled to.

One best practice to strongly consider is setting up weekly cloud cost reports that go to the leadership team. Also, be prepared to occasionally renegotiate your cloud services contract so it’s as straightforward as possible and optimally suited to your business’s needs.

Don’t give up

To be clear, controlling IT costs should never mean cutting corners or scrimping on mission-critical technology expenses — particularly those related to cybersecurity. That said, you also should never give up on managing your IT budget. FMD can help you develop a tailored cost-control strategy that keeps your technology current and supports your business objectives.

Stepped-Up Basis Rules Can Ease the Income Tax Bite of an Inheritance

With the federal gift and estate tax exemption amount set at $13.99 million for 2025, most people won’t be liable for these taxes. However, capital gains tax on inherited assets may cause an unwelcome tax bite.

The good news is that the stepped-up basis rules can significantly reduce capital gains tax for family members who inherit your assets. Under these rules, when your loved one inherits an asset, the asset’s tax basis is adjusted to the fair market value at the time of your death. If the heir later sells the asset, he or she will owe capital gains tax only on the appreciation after the date of death rather than on the entire gain from when you acquired it.

Primer on capital gains tax

When assets such as securities are sold, any resulting gain generally is a taxable capital gain. The gain is taxed at favorable rates if the assets have been owned for longer than one year. The maximum tax rate on a long-term capital gain is 15% but increases to 20% for certain high-income individuals.

Conversely, a short-term capital gain is taxed at ordinary income tax rates as high as 37%. Gains and losses are accounted for when filing a tax return, so high-taxed gains may be offset wholly or partially by losses.

The amount of a taxable gain is equal to the difference between the basis of the asset and the sale price. For example, if you acquire stock for $10,000 and then sell it for $50,000, your taxable capital gain is $40,000.

These basic rules apply to capital assets owned by an individual and sold during his or her lifetime. However, a different set of rules applies to inherited assets.

How stepped-up basis works

When assets are passed on through inheritance, there’s no income tax liability until the assets are sold. For these purposes, the basis for calculating gain is “stepped up” to the value of the assets on the date of your death. Thus, only the appreciation in value since your death is subject to tax because the individual inherited the assets. The appreciation during your lifetime goes untaxed.

Securities, artwork, bank accounts, business interests, investment accounts, real estate and personal property are among the assets affected by the stepped-up basis rules. However, these rules don’t apply to retirement assets such as 401(k) plans or IRAs.

To illustrate the benefits, let’s look at a simplified example. Dan bought XYZ Corp. stock 10 years ago for $100,000. In his will, he leaves all the XYZ stock to his daughter, Alice. When Dan dies, the stock is worth $500,000. Alice’s basis is stepped up to $500,000.

When Alice sells the stock two years later, it’s worth $700,000. She must pay the maximum 20% rate on her long-term capital gain. On these facts, Alice has a $200,000 gain. With the 20% capital gains rate, she owes $40,000. Without the stepped-up basis, her tax on the $600,000 gain would be $120,000.

What happens if an asset declines in value after the deceased acquired it? The adjusted basis of the asset the individual inherits is still the value on the date of death. This could result in a taxable gain on a subsequent sale if the value rebounds after death, or a loss if the asset’s value continues to decline.

Turn to us for help

Without the stepped-up basis rules, your beneficiaries could face much higher capital gains taxes when they sell their inherited assets. If you have questions regarding these rules, please contact FMD.

Growing the Business Means Supporting your Managers

Many different shortcomings can hold back the growth of a company. Some are obvious, such as poor cash flow management or flawed strategic plans. Others aren’t so easy to see.

Take, for example, disjointed or under-supported managers. If you don’t dedicate the time and resources to strengthening the bonds of your management team, and provide the support they need, your company may struggle with slower growth as a consequence.

Follow a collaborative approach

A good place to start is by making sure you’re following a collaborative approach to running the business. Develop strategic goals with your management team’s input and buy-in so everyone is pulling in the same direction. From there, actively work to keep managers engaged in meeting department-specific objectives related to strategic goals.

Collaboration has other benefits, too. More individuals participating in decision-making can mean more creative and well-thought-out solutions. A collaborative approach also distributes the burden of strategic planning so it doesn’t fall on only your shoulders. Sharing responsibility for key decisions — particularly as a business grows — is vital to facilitating progress and seizing opportunities.

Build an accessible knowledge base

Involving managers in decision-making calls for developing a robust, accessible knowledge base about your company’s product or service lines, organizational structure, market, customer base and operating environment. Your management team must be able to view, in real time, the information they need to contribute to strategic planning and guide their departments.

The good news is that today’s technology allows you to create a centralized platform for authorized users to share and access critical data so everyone is on the same page. For example, you can use enterprise resource planning software to gather, store and analyze business intelligence related to core processes such as human resources, financial management and reporting, and supply chain management. You can integrate customer relationship management software to track and share data related to customers, prospects and key contacts.

When in doubt, conduct an assessment

If you’re unsure where your management team stands, you may want to perform a formal assessment. This entails undertaking a thorough and confidential review of every manager to identify issues — whether cultural, technical or interpersonal — that may be detracting from team performance.

To help ensure objectivity, many businesses engage outside consultants specializing in executive or leadership development to perform such assessments. The assessments generally consist of live or virtual interviews, sometimes in group settings, and written or online evaluations. The goal is to gain insights into:

Individual and group strengths and weaknesses,

Team dynamics,

Barriers to success,

Areas of improvement, and

Untapped opportunities.

Assessment providers typically issue results in written reports and debriefing sessions. Most will help you create an action plan to make use of the information gathered.

Consider an annual retreat

To take management team building to the next level, you may want to hold annual retreats. Doing so can be particularly important following one of the aforementioned assessments.

Management retreats typically follow a more intense format than company-wide team-building events. Ways to structure each retreat are limited only by budget, creativity and perhaps team members’ physical limitations. The goal is to break down functional silos and communication barriers and build up a greater sense of trust and unity.

However, to fully realize the potential value of a retreat, you must follow up. That means harnessing the experiences and breakthroughs that occur during the event and using them to create an action plan for improving management performance back at the office. (If you’ve also conducted a management team assessment, you can combine the two action plans.)

Give them support

It’s all too easy for managers to get caught up in their respective departments’ day-to-day trials and travails. That’s how growth inhibitors such as knowledge silos and leadership conflicts happen. Give your management team the encouragement and support it deserves. FMD can help you identify and analyze all the costs of performance development at every level of your business.

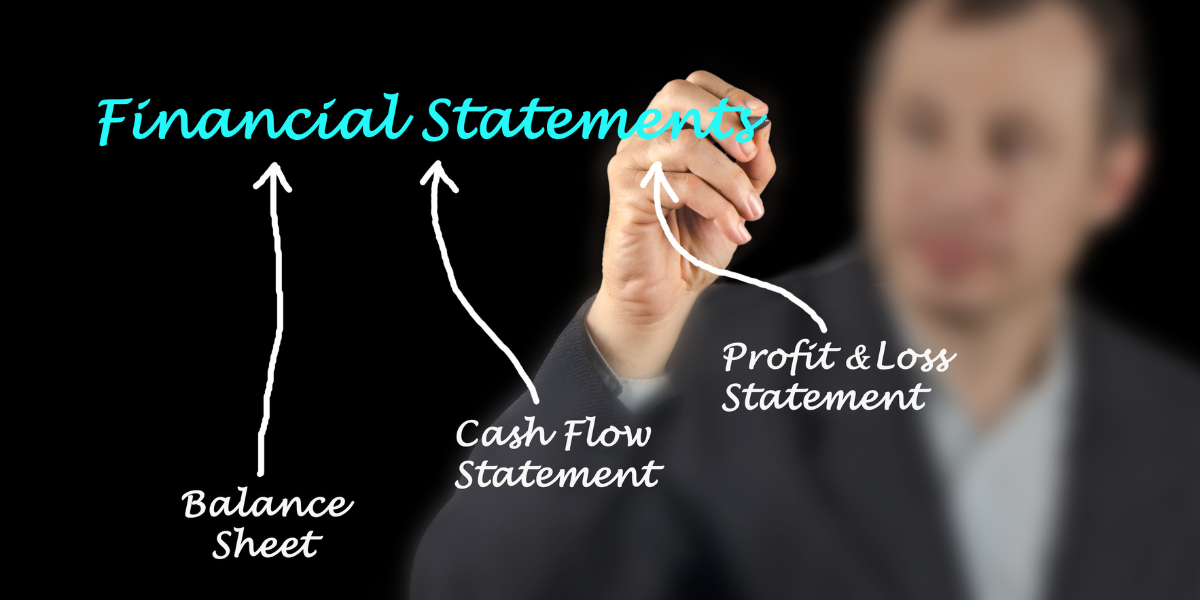

Business Owners Should Get Comfortable with their Financial Statements

Financial statements can fascinate accountants, investors and lenders. However, for business owners, they may not be real page-turners.

The truth is each of the three parts of your financial statements is a valuable tool that can guide you toward reasonable, beneficial business decisions. For this reason, it’s important to get comfortable with their respective purposes.

The balance sheet

The primary purpose of the balance sheet is to tally your assets, liabilities and net worth, thereby creating a snapshot of your business’s financial health during the statement period.

Net worth (or owners’ equity) is particularly critical. It’s defined as the extent to which assets exceed liabilities. Because the balance sheet must balance, assets need to equal liabilities plus net worth. If the value of your company’s liabilities exceeds the value of its assets, net worth will be negative.

In terms of operations, just a couple of balance sheet ratios worth monitoring, among many, are:

Growth in accounts receivable compared with growth in sales. If outstanding receivables grow faster than the rate at which sales increase, customers may be taking longer to pay. They may be facing financial trouble or growing dissatisfied with your products or services.

Inventory growth vs. sales growth. If your business maintains inventory, watch it closely. When inventory levels increase faster than sales, the company produces or stocks products faster than they’re being sold. This can tie up cash. Moreover, the longer inventory remains unsold, the greater the likelihood it will become obsolete.

Growing companies often must invest in inventory and allow for increases in accounts receivable, so upswings in these areas don’t always signal problems. However, jumps in inventory or receivables should typically correlate with rising sales.

Income statement

The purpose of the income statement is to assess profitability, revenue generation and operational efficiency. It shows sales, expenses, and the income or profits earned after expenses during the statement period.

One term that’s commonly associated with the income statement is “gross profit,” or the income earned after subtracting cost of goods sold (COGS) from revenue. COGS includes the cost of labor and materials required to make a product or provide a service. Another important term is “net income,” which is the income remaining after all expenses — including taxes — have been paid.

The income statement can also reveal potential problems. It may show a decline in gross profits, which, among other things, could mean production expenses are rising more quickly than sales. It may also indicate excessive interest expenses, which could mean the business is carrying too much debt.

Statement of cash flows

The purpose of the statement of cash flows is to track all the sources (inflows) and recipients (outflows) of your company’s cash. For example, along with inflows from selling its products or services, your business may have inflows from borrowing money or selling stock. Meanwhile, it undoubtedly has outflows from paying expenses, and perhaps from repaying debt or investing in capital equipment.

Although the statement of cash flows may seem similar to the income statement, its focus is solely on cash. For instance, a product sale might appear on the income statement even though the customer won’t pay for it for another month. But the money from the sale won’t appear as a cash inflow until it’s collected.

By analyzing your statement of cash flows, you can assess your company’s ability to meet its short-term obligations and manage its liquidity. Perhaps most importantly, you can differentiate profit from cash flow. A business can be profitable on paper but still encounter cash flow issues that leave it unable to pay its bills or even continue operating.

Critical insights

You can probably find more exciting things to read than your financial statements. However, you won’t likely find anything more insightful regarding how your company is performing financially. FMD can help you not only generate best-in-class financial statements, but also glean the most valuable information from them.

Family Business Focus: Taking it to The Next Level

Family businesses often start out small, with casual operational approaches. However, informal (or nonexistent) policies and procedures can become problematic as such companies grow.

Employees may grumble about unclear, inconsistent rules. Lenders and investors might frown on suboptimal accounting practices. Perhaps worst of all, customers can become disenfranchised by slow or unsatisfying service. Simply put, there may come a time when you have to take it to the next level.

4 critical areas

Has your family-owned company reached the point where it needs to expand its operational infrastructure to handle a larger customer base, manage higher revenue volumes and capitalize on new market opportunities? If so, look to strengthen these four critical areas:

1. Performance management. Family business owners often get used to putting out fires and tying up loose ends. However, as the company grows, doing so can get increasingly difficult and frustrating. Sound familiar? The problem may not lie entirely with your employees. If you haven’t already done so, write formal job descriptions. Then, provide proper training to teach staff members how to fulfill the stated duties.

From there, implement a formal performance management system to evaluate employees, give constructive feedback, and help determine promotions and pay raises. Effective performance management not only helps employees improve, but also contributes to motivation and retention. It’s particularly important for nonfamily staff, who may feel like they’re not being evaluated the same way as working family members.

In addition, if you don’t yet have an employee handbook, write one. Work with a qualified employment attorney to refine the language and ask everyone to sign an acknowledgment that they received and read it.

2. Business processes. Think of your business processes as the pistons of the engine that drives your family-owned company. We’re talking about things such as:

Production of goods or services,

Sales and marketing,

Customer support,

Accounting and financial management, and

Human resources.

The more you document and enhance these and other processes, the easier it is to train staff and improve their performances. Bear in mind that enhancing business processes usually involves streamlining them to reduce manual effort and redundancies.

3. Strategic planning. Many family business owners keep their company visions to themselves. If they do share them, it’s impromptu, around the dinner table or during family gatherings.

As your company grows, formalize your approach to strategic planning. This starts with building a solid leadership team with whom you can share your thoughts and listen to their opinions and ideas. From there, hold regular strategic-planning meetings and perhaps even an annual retreat.

When ready, share company goals with employees and ask for their feedback. Keeping staff in the loop empowers them and helps ensure they buy into the direction you’re taking.

4. Information technology. Nowadays, the systems and software your family business uses to operate can make or break its success. As your company grows, outdated or unscalable solutions will likely inhibit efficiency, undercut competitiveness, and expose you to fraud or hackers.

Running a professional, process-oriented business generally requires integration. This means all your various systems and software should work together seamlessly. You want your authorized users to be able to get to information quickly and easily. You also want to automate as many processes as possible to improve efficiency and productivity.

Last but certainly not least, you must address cybersecurity. Growing family businesses are prime targets for criminals looking to steal data or abduct it for ransom. Internal fraud is an ever-present threat as well.

Change and adapt

Perhaps the most dangerous thing any family business owner can say is, “But we’ve always done it that way!” A growing company is a testament to your hard work, but you’ll need to be adaptable and willing to change to keep it moving forward. FMD can help you reevaluate and improve all your business processes related to accounting, financial management and tax planning.

Incentive Trusts: Use Them to Pass your Wealth and Values on to Beneficiaries

If your estate planning goals include distributing your wealth while also encouraging specific behaviors or achievements among your heirs, using an incentive trust might be right for your plan.

Unlike a traditional trust, which distributes assets according to a set schedule or upon a beneficiary reaching a certain age, an incentive trust includes specific conditions that must be met before distributions are made. These conditions can align with your values, such as pursuing higher education, maintaining gainful employment, engaging in charitable work or avoiding destructive behaviors like substance abuse.

Setting guidelines

Essentially, an incentive trust sets guidelines for how a beneficiary becomes eligible to benefit from the trust. Distributions can, for instance, be contingent on a beneficiary graduating from high school, earning certain grades, or enrolling in or graduating from college.

Then again, perhaps you’re more concerned about a beneficiary’s physical well-being than his or her intellectual one. In this case, you might structure an incentive trust to disallow payouts if the beneficiary indulges in harmful or illegal behavior, such as abusing alcohol or using illegal drugs. Going this route will, however, require that you appoint a trustee who knows the issues and who can monitor the beneficiary’s activities and enforce the provision.

From a business perspective, an incentive trust can include provisions that reward your beneficiary for becoming involved in the family business or mapping out a career path of his or her own. Build in matching charitable donations and you can help the beneficiary develop an appreciation for community service and volunteerism.

Minding the risks

Incentive trusts come with some inherent risks. If the provisions are too restrictive, or simply don’t suit the beneficiary in question, the incentive may backfire.

For instance, say Jane, a 20-year-old college dropout, learns that her Aunt Lucy has provided her with $500,000 in trust. However, Jane can withdraw the trust funds only if she returns to college and earns a bachelor’s degree.

The problem is, Jane never really liked Aunt Lucy, who often scolded her for making bad choices and meddled in her life. And Jane didn’t really like college either. As a result, the trust only furthers Jane’s resolve to never return to college — no matter how much money she loses.

In other cases, the beneficiary may force him- or herself to complete a degree but wind up living an unfulfilled life because he or she had other dreams in mind. Or you might end up “motivating” a beneficiary to work for the family business when he or she really doesn’t want to, which, in turn, could hurt the company.

Communicating with clarity

A big part of making sure an incentive trust will work is clearly communicating with your trustee. He or she should generally have broad discretionary powers because, as time passes, a beneficiary’s circumstances might change. For example, a student might develop learning or other disabilities that prevent him or her from achieving the academic goals set by the incentive provisions.

In general, the trust should provide enough of a safety net that, if the beneficiary fails to achieve the trust’s goals, he or she will still be able to support him- or herself. The incentive provisions can apply to only a part of the trust assets. The trust should also provide for giving some or all the funds to a secondary beneficiary, in case the primary beneficiary fails to meet the stated goals or dies.

Contact FMD if you have questions regarding an incentive trust.

Estate planning Q&A: Guardianship

If you’re the parent of a newborn, toddler or older child, you may be thinking about naming a guardian for him or her. This can be a difficult decision, especially if you have many choices or, on the other hand, no one you can trust.

The following are answers to common questions about guardianship:

Q. How do I choose a guardian for my child?

A. In most cases involving a single parent or a parenting couple, you designate the guardian in a legally valid will. This means the guardian will raise your child if you (or you and your partner) should die unexpectedly. A similar provision may address incapacitation issues.

Choose the best person for the job and designate an alternate in case your first choice can’t fulfill the duties. Parents frequently name a married couple who are relatives or close friends. If you take this approach, ensure both spouses have legal authority to act on the child’s behalf.

Also, select someone who has the necessary time and resources for this immense responsibility. Although it’s usually not recommended, you can name different guardians for different children.

In addition, consider the living arrangements and the geographic area where your child would reside if the guardian assumed legal responsibilities. Do you really want to uproot your child and send him or her to live somewhere far away from familiar surroundings?

Q. Do I have to justify my decision?

A. No. However, it can’t hurt — and it could help — to prepare a letter of explanation for the benefit of any judge presiding over a guardianship matter for your family. The letter can provide insights into your choice of guardian.

Notably, the judge will apply a standard based on the child’s “best interests,” so you should explain why the guardian you’ve named is the optimal choice. Focus on aspects such as the child’s preferences, who can best meet the child’s needs, the moral and ethical character of the potential guardian, and the guardian’s relationship to the child.

Whether you’re naming a guardian for a child in your will or you’re attempting to become a guardian yourself, you must adhere to the legal principles under state and local law. Fortunately, FMD can provide any necessary guidance.

Weighing the Pluses and Minuses of HDHPs + HSAs for Businesses

Will your company be ready to add a health insurance plan for next year, or change its current one? If so, now might be a good time to consider your options. These things take time.

A popular benefits model for many small to midsize businesses is sponsoring a high-deductible health plan (HDHP) accompanied by employee Health Savings Accounts (HSAs). Like any such strategy, however, this one has its pluses and minuses.

Ground rules

HSAs are participant-owned, tax-advantaged accounts that accumulate funds for eligible medical expenses. To own an HSA, participants must be enrolled in an HDHP, have no other health insurance and not qualify for Medicare.

In 2025, an HDHP is defined as a plan with at least a $1,650 deductible for self-only coverage or $3,300 for family coverage. Also in 2025, participants can contribute pretax income of up to $4,300 for self-only coverage or $8,550 for family coverage. (These amounts are inflation-adjusted annually, so they’ll likely change for 2026.) Those age 55 or older can make additional catch-up contributions of $1,000.

Companies may choose to make tax-deductible contributions to employees’ HSAs. However, the aforementioned limits still apply to combined participant and employer contributions.

Participants can make tax-free HSA withdrawals to cover qualified out-of-pocket medical expenses, such as physician and dentist visits. They may also use their account funds for copays and deductibles, though not to pay many types of insurance premiums.

Pluses to ponder

For businesses, the “HDHP + HSAs” model offers several pluses. First, HDHPs generally have lower premiums than other health insurance plans — making them more cost-effective. Plus, as mentioned, your contributions to participants’ HSAs are tax deductible if you choose to make them. And, overall, sponsoring health insurance can strengthen your fringe benefits package.

HSAs also have pluses for participants that can help you “sell” the model when rolling it out. These include:

Participants can lower their taxable income by making pretax contributions through payroll deductions,

HSAs can include an investment component that may include mutual funds, stocks and bonds,

Account earnings accumulate tax-free,

Withdrawals for qualified medical expenses aren’t subject to tax, and the list of eligible expenses is extensive,

HSA funds roll over from year to year (unlike Flexible Spending Account funds), and

HSAs are portable; participants maintain ownership and control of their accounts if they change jobs or even during retirement.

In fact, HSAs are sometimes referred to as “medical IRAs” because these potentially valuable accounts are helpful for retirement planning and have estate planning implications as well.

Minuses to mind

The HDHP + HSAs model has its minuses, too. Some employees may strongly object to the “high deductible” aspect of HDHPs.

Also, if not trained thoroughly, participants can misuse their accounts. Funds used for nonqualified expenses are subject to income taxes. Moreover, the IRS will add a 20% penalty if an account holder is younger than 65. After age 65, participants can withdraw funds for any reason without penalty, though withdrawals for nonqualified expenses will be taxed as ordinary income.

Expenses are another potential concern. HSA providers (typically banks and investment firms) may charge monthly maintenance fees, transaction fees and investment fees (for accounts with an investment component). Many companies cover these fees under their benefits package to enhance the appeal of HSAs to employees.

Finally, HSAs can have unexpected tax consequences for account beneficiaries. Generally, if a participant dies, account funds pass tax-free to a spouse beneficiary. However, for other types of beneficiaries, account funds will be considered income and immediately subject to taxation.

Powerful savings vehicle

The HDHP + HSAs model helps businesses manage insurance costs, shifts more of medical expense management to participants, and creates a powerful savings vehicle that may attract job candidates and retain employees. But that doesn’t mean it’s right for every company. Please contact FMD for help assessing its feasibility, as well as identifying the cost and tax impact.

Estate Planning for Residential Real Estate with a Qualified Personal Residence Trust

Do you own your principal residence? If so, you’re likely aware that you can benefit from the home’s build-up in equity, realize current tax breaks and pocket a sizable tax-exempt gain when you sell it.

And from an estate planning perspective, it may be beneficial to transfer ownership of your home to a qualified personal residence trust (QPRT). Using a QPRT, you can continue to live in the home for the duration of the trust’s term. When the term ends, the remainder interest passes to designated beneficiaries.

A QPRT in action

When you transfer a home to a QPRT, it’s removed from your taxable estate. The transfer of the remainder interest is subject to gift tax, but tax resulting from this future gift is generally reasonable. The IRS uses the Section 7520 rate, which is updated monthly, to calculate the tax. For September 2024, the rate is 4.8%, down from the year’s high thus far of 5.6% in June.

You must appoint a trustee to manage the QPRT. Frequently, the grantor will act as the trustee. Alternatively, it can be another family member, friend or professional advisor.

Typically, the home being transferred to the QPRT is your principal residence. However, a QPRT may also be used for a second home, such as a vacation house.

What happens if you die before the end of the trust’s term? Then the home is included in your taxable estate. Although this defeats the intentions of the trust, your family is no worse off than it was before you created the QPRT.

There’s no definitive period of time for the trust term, but the longer the term, the smaller the value of the remainder interest for tax purposes. Avoid choosing a term longer than your life expectancy. Doing so will reduce the chance that the home will be included in your estate should you die before the end of the term. If you sell the home during the term, you must reinvest the proceeds in another home that will be owned by the QPRT and subject to the same trust provisions.

So long as you live in the residence, you must continue to pay the monthly bills, including property taxes, maintenance and repair costs, and insurance. Because the QPRT is a grantor trust, you’re entitled to deduct qualified expenses on your tax return, within the usual limits.

Potential drawbacks

When a QPRT’s term ends, the trust’s beneficiaries become owners of the home, at which point you’ll need to pay them a fair market rental rate if you want to continue to live there. Despite the fact that it may feel strange to have to pay rent to live in “your” home, at that point, it’s no longer your home. Further, paying rent generally coincides with the objective of shifting more assets to younger loved ones.

Note, also, that a QPRT is an irrevocable trust. In other words, you can’t revise the trust or back out of the deal. The worst that can happen is you pay rent to your beneficiaries if you outlive the trust’s term, or the home reverts to your estate if you don’t. Also, the beneficiaries will owe income tax on any rental income.

Contact FMD to determine if a QPRT is right for your estate plan.

Beneficial Ownership Information Reporting Requirements Suspended for Domestic Reporting Companies

The twisty journey of the Corporate Transparency Act’s (CTA’s) beneficial ownership information (BOI) reporting requirements has taken yet another turn. Following a February 18, 2025, ruling by a federal district court (Smith v. U.S. Department of the Treasury), the requirements are technically back in effect for covered companies. But a short time later, the U.S. Department of the Treasury announced it would suspend enforcement of the CTA against domestic reporting companies and U.S. citizens. Here are the latest developments and what they may mean for you.

Latest announcement

On March 2, the Treasury Department stated the following in a press release: “The Treasury Department is announcing today that, with respect to the Corporate Transparency Act, not only will it not enforce any penalties or fines associated with the beneficial ownership information reporting rule under the existing regulatory deadlines, but it will further not enforce any penalties or fines against U.S. citizens or domestic reporting companies or their beneficial owners after the forthcoming rule changes take effect either. The Treasury Department will further be issuing a proposed rulemaking that will narrow the scope of the rule to foreign reporting companies only. Treasury takes this step in the interest of supporting hard-working American taxpayers and small businesses and ensuring that the rule is appropriately tailored to advance the public interest.”

The reinstatement

On January 23, 2025, the U.S. Supreme Court granted the government’s motion to stay, or halt, a nationwide injunction issued by a federal court in Texas (Texas Top Cop Shop, Inc. v. Bondi). But a separate nationwide order from the Smith court was still in place until February 18, 2025, so the reporting requirements remained on hold. With that order now stayed, the new deadline to file a BOI report with the U.S. Treasury Department’s Financial Crimes Enforcement Network (FinCEN) is technically March 21, 2025.

Reporting companies that were previously given a reporting deadline later than this deadline are required to file their initial BOI report by the later deadline. For example, if a company’s reporting deadline is in April 2025 because it qualifies for certain disaster relief extensions, it’s allowed to follow the April deadline rather than the March deadline.

Important: Due to ongoing litigation in another federal district court (National Small Business United v. Yellen), members of the National Small Business Association as of March 1, 2024, aren’t currently required to report their BOI to FinCEN.

BOI requirements in a nutshell

The BOI requirements are intended to help prevent criminals from using businesses for illicit activities, such as money laundering and fraud hidden through shell companies or other opaque ownership structures. Companies covered by the requirements are referred to as “reporting companies.”

Such businesses have been reporting certain identifying information on their beneficial owners. FinCEN estimated that approximately 32.6 million companies would be affected by the reporting rules in the first year.

Beneficial owners are defined as natural persons who either directly or indirectly 1) exercise substantial control over a reporting company, or 2) own or control at least 25% of a reporting company’s ownership interests. Individuals who exercise substantial control include senior officers, important decision makers, and those with authority to appoint or remove certain officers or a majority of the company’s governing body.

For each beneficial owner, under the requirements, a reporting company must provide the individual’s:

Name,

Date of birth,

Residential address, and

Identifying number from an acceptable identification document, such as a passport or U.S. driver’s license, and the name of the issuing state or jurisdiction of the identification document.

A reporting company also must submit an image of the identification document.

BOI reporting isn’t an annual obligation. However, companies must report any changes to the required information previously reported about their businesses or beneficial owners. Updated reports are due no later than 30 days after the date of the change.

Stay tuned

The temporary stay of the injunction in the Smith case applies only until the U.S. Court of Appeals for the Fifth Circuit rules on FinCEN’s appeal of the lower court’s original injunction order in that case. The appeal was filed on February 5, 2025. Additional challenges are also proceeding in other courts. It’s also possible that Congress will pass legislation to repeal the BOI requirements.

Meanwhile, the March 2 Treasury announcement appears to ease compliance concerns for domestic companies. However, FinCEN will continue to enforce requirements for foreign reporting companies. Contact FMD if you have questions about your situation.

Estate Planning for Non-U.S. Citizens Requires Extra Care

Traditional estate planning strategies generally are based on the assumption that all family members involved are U.S. citizens. However, if you or your spouse is a noncitizen, special rules apply that require additional planning. Avoid costly tax traps by understanding how the U.S. gift and estate tax laws apply to noncitizens.

Defining “domicile”

Noncitizens can become subject to U.S. gift and estate taxes if they’re domiciled in the United States. Under IRS guidelines, an individual becomes domiciled in a country “by living there, for even a brief period of time, with no definite present intention of later removing therefrom.”

To determine a person’s “present intention,” the IRS considers a number of factors, such as the amount of time the person spends in the United States; their green card or visa status; the location of their business interests and residences; the location of their health care providers, jobs, places of worship and community ties; the place where their vehicles are registered and where they’re licensed to drive; the place where they’re registered to vote; and the domiciles of their friends and family members.

Noncitizens who are deemed to be domiciled in the United States are subject to U.S. gift and estate taxes on their worldwide assets, much like U.S. citizens. And, like U.S. citizens, they’re eligible for the federal gift and estate tax exemption ($13.99 million for 2025) and the annual gift tax exclusion ($19,000 per recipient for 2025).

A significant difference between U.S. citizens and noncitizens, and a potential tax trap for the unwary, is that the marital deduction isn’t available for transfers to noncitizens. Ordinarily, married couples can transfer an unlimited amount of assets between each other — during their lifetimes or at death — without triggering gift or estate taxes. However, estate planning strategies that rely on the marital deduction may not be available to noncitizen domiciliaries.

There are other options, however. For example, a spouse can:

Make tax-free transfers to his or her noncitizen spouse up to the transferor’s unused gift and estate tax exemption.

Make annual exclusion gifts. The annual exclusion for gifts to a noncitizen spouse is $190,000 for 2025.

Potential tax trap

A person who’s neither a U.S. citizen nor a U.S. domiciliary — that is, a “nonresident alien” — is subject to U.S. gift and estate taxes only on assets that are “situated” in the United States. Intangible property — such as corporate stock, bonds or promissory notes — is deemed to be situated in the United States for estate tax purposes (but typically not for gift tax purposes) if it’s issued by a domestic corporation or by a U.S. citizen or the U.S. government.

Here’s where the potential tax trap comes into play: The exemption amount for U.S.-situated assets owned by nonresident aliens is only $60,000, compared with $13.99 million for U.S. citizens or domiciliaries. Depending on the value of a person’s property in the United States, this can result in significant gift and estate taxes.

There may be strategies for avoiding these taxes, such as holding the assets through a properly structured and operated foreign corporation. Also, in some cases, tax treaties between the United States and a nonresident alien’s country of citizenship may provide some relief.

If you or your spouse is a noncitizen, talk to FMD about the potential estate planning ramifications.

Disaster Victims may Qualify for Tax Relief … Including on Amended Returns

Victims of presidentially declared disasters in recent years who couldn’t previously claim a casualty loss deduction may now be able to claim a refund. Additional tax relief also might be available. Read on to learn more about the potential opportunities for victims of certain disasters.

Loosened restrictions for casualty losses

The tax relief comes via the Federal Disaster Tax Relief Act (FDTRA), which was signed into law by former President Biden in December 2024. Among other things, the law makes it easier to claim a deduction for qualified disaster-related personal casualty losses during a specific time period.

Previously, you could claim such a deduction only if you itemized your deductions. It was further limited by a $100 reduction per loss, and you were allowed to deduct only the amount of the loss that exceeded 10% of your adjusted gross income. The so-called 10% rule was applied after the $100 reduction.

Under the FDTRA, those restrictions no longer apply if you suffered a casualty loss attributable to a presidentially declared disaster (referred to as a “qualified disaster loss”) that began on or after December 28, 2019, and on or before December 12, 2024, and ended no later than January 11, 2025. (Note that this relief doesn’t apply to the 2025 California wildfires. See “Wildfire relief” below for information on other relief available to the victims of those and other more recent fires.)

In addition, the president must have made the disaster declaration between January 1, 2020, and February 10, 2025. The limit for such losses is that each separate casualty loss is deductible only after it exceeds $500.

Be aware that casualty losses are generally deductible in the year the loss is incurred. For example, if a qualified disaster occurred in 2022, but your insurance company didn’t deny your related claim until 2024, you’d deduct the loss for 2024. But you now have the option to deduct any loss attributable to a presidentially declared disaster in the tax year prior to the occurrence.

Wildfire relief

The FDTRA provides that “qualified wildfire relief payments” — including those made to Los Angeles County taxpayers affected by the 2025 California wildfires — can be excluded from gross income for tax purposes. It’s been estimated that this provision will return $512 million in taxes to wildfire victims. And it’ll protect payment recipients from losing certain income-based benefits, such as health insurance premium subsidies, Veterans Administration co-pay assistance and federal student aid.

The exclusion applies to any amount received by, or on behalf of, an individual as compensation for losses, expenses or damages, including for:

Additional living expenses,

Lost wages, other than compensation for lost wages paid by the employer which otherwise would have paid those wages,

Personal injury,

Death, and

Emotional distress.

The compensation must have been granted for a federally declared disaster that was declared after December 31, 2014, as the result of a forest or range fire. The payments must be received during tax years beginning after December 31, 2019, and before January 1, 2026. Compensation from insurance and other reimbursements doesn’t qualify for the exclusion.

The law prohibits double-dipping. You can’t claim a deduction or credit for any expense excluded from income under the provision. And, if you use excluded qualified payments to purchase or improve property, you may not increase your basis or adjusted basis in the property by the excluded amount.

The IRS is also providing some relief related to filing deadlines for individuals and households that reside or have a business in Los Angeles County and were affected by wildfires and straight-line winds that began on January 7, 2025. These taxpayers have until October 15, 2025, to file various federal individual and business tax returns and make tax payments.

The new deadline applies to individual income tax returns and payments normally due on April 15, 2025. This relief also applies to the 2024 estimated tax payment that was due on January 15, 2025, and estimated tax payments normally due on April 15, June 16, and September 15, 2025.

It also applies to:

Quarterly payroll and excise tax returns normally due on January 31, April 30, and July 31, 2025,

Calendar-year partnership and S corporation returns normally due on March 17, 2025,

Calendar-year corporation and fiduciary returns and payments normally due on April 15, 2025, and

Calendar-year tax-exempt organization returns normally due on May 15, 2025.

East Palestine train derailment relief

The FDTRA also extends relief to victims of the train derailment on February 3, 2023, in East Palestine, Ohio. “East Palestine Train Derailment Payments” can be excluded from gross income.

The payments include any amount received by, or on behalf of, an individual as derailment-related compensation for:

Loss,

Damages,

Expenses,

Loss in real property value,

Closing costs related to real property (including realtor commissions), and

Inconvenience (including access to real property).

The compensation must have come from a federal, state or local government agency, Norfolk Southern Railway, or any subsidiary, insurer or agent of Norfolk Southern Railway.

Next steps for taxpayers

If you’re claiming any of the benefits under the FDTRA for a tax year for which you’ve already filed a tax return without claiming the benefits, you’ll need to file an amended return. We can file your amended return electronically if you’re amending a return for the current or prior two tax periods.

You must file Form 1040-X, Amended U.S. Individual Income Tax Return, on paper to amend your return if 1) the amended return is for earlier years, or 2) your prior year return was originally filed on paper during the current processing year. If you file your amended return electronically, you can elect to have any refund directly deposited into a U.S. financial institution account. Contact FMD with any questions and to prepare an amended return for you.

ESOPs can Help Business Owners with Succession Planning

Devising and executing the right succession plan is challenging for most business owners. In worst-case scenarios, succession planning is left to chance until the last minute. Chaos, or at least much confusion and uncertainty, often follows.

The most foolproof way to make succession planning easier is to give yourself plenty of time to develop a plan that suits the intricacies of your situation and then gradually implement it. One vehicle that can help “slow your roll” into retirement or whatever your next stage of life may be is an employee stock ownership plan (ESOP).

Little by little

An ESOP is a type of qualified retirement plan that invests solely or mainly in your company’s stock. Because it’s qualified, an ESOP comes with tax advantages as long as you follow the federally enforced rules. These include requirements related to minimum coverage and contribution limits.

Generally, the company sets up an ESOP trust and funds the plan by contributing shares or cash to buy existing shares. Distributions to eligible participants are made in stock or cash. For closely held companies, employees who receive stock have the right to sell it back to the company — exercising “put options” or an “option to sell” — at fair market value during certain time windows.

Although an ESOP involves transferring ownership to employees, it’s different from a management or employee buyout. Unlike a buyout, an ESOP allows owners to cash out and transfer control little by little. During the transfer period, owners’ shares are held in the ESOP trust and voting rights on most issues other than mergers, dissolutions and other major transactions are exercised by the trustees, who may be officers or other company insiders.

Appraisals required

One big difference between ESOPs and other qualified retirement plans, such as 401(k)s, is mandated valuations. The Employee Retirement Income Security Act requires trustees to obtain appraisals by independent valuation professionals to support ESOP transactions. Specifically, an appraisal is needed when the ESOP initially acquires shares from the company’s owners and every year thereafter that the business contributes to the plan.

The fair market value of the sponsoring company’s stock is important because the U.S. Department of Labor specifically prohibits ESOPs from paying more than “adequate consideration” when investing in employer securities. In addition, because employees who receive ESOP shares typically have the right to sell them back to the company at fair market value, the ESOP provides a limited market for its shares.

Drawbacks to consider

An ESOP can play a helpful role in a well-designed succession plan with an appropriately long timeline. However, there are potential drawbacks to consider. You’ll incur costs and considerable responsibilities related to plan administration and compliance. Costs are also associated with annual stock valuations and the need to repurchase stock from employees who exercise put options.

Another potential disadvantage is that ESOPs are available only to corporations of either the C or S variety. Limited liability companies, partnerships and sole proprietorships must convert to one of these two entity types to establish an ESOP. Doing so will raise a variety of tax and financial issues.

In addition, it’s important to explore the potential negative impact of ESOP debt and other expenses on your financial statements and ability to qualify for loans.

Not a no-brainer

ESOPs have become fairly popular among small to midsize businesses. However, the decision to create, launch and administer one is far from a no-brainer. You’ll need to do a deep dive into all the details involved, discuss the concept with your leadership team and get professional advice. Contact FMD for help evaluating whether an ESOP would be a good fit for your business and succession plan.

What Happens if You and Your Siblings Inherit your Parents’ Home?

When estate planning, it’s common for parents to leave their primary residence or a vacation home to their children. While your parents’ wills or trusts may specify who gets what percentage of the home, typically, you and your siblings will receive equal shares in the property.

This can result in potential problems. For example, perhaps you and your siblings have different financial needs or can’t agree on what to do with the home. Let’s take a look at how to best approach the situation.

Determine what to do with the house

The first step is to sit down with your siblings and have an open, honest discussion about your wishes for handling the inherited home. Generally, the options are:

Keep the home and share it among family members,

Rent out the home and share the rental income,

Sell the home and divide the profits, or

Arrange for one sibling to buy out the others.

If you decide to share the home, have a written agreement drafted by your attorney that outlines rules regarding scheduling, allowable uses, and responsibility for maintenance and expenses. If you choose to sell the home or arrange a buyout, obtain a professional appraisal to avoid disputes over the home’s value.

Other considerations

If you rent out the home, determine how you’ll handle rent collection, maintenance and other rental activities. One option is to engage a property management company to handle the day-to-day management.

Another issue to consider is how the title to the property will be held. For example, if you and your siblings own the home as tenants in common, then your respective interests will pass to your heirs according to your individual estate plans. But if you hold the property as joint tenants, then when one sibling dies, the surviving siblings receive his or her share.

Keep in mind that each of the options described above has different tax implications. Contact FMD with questions.

Embrace the Future: Sales Forecasting for Businesses

So, how are sales looking for next year? It’s not a rhetorical question. Your business should be able to look ahead and accurately estimate how its future sales are shaping up. This practice is called sales forecasting, and doing it well is key to better managing your company’s financial performance.

Why it’s important

Formally defined, sales forecasting is a comprehensive process for estimating future revenue in a given period based on carefully chosen metrics and, often, human input.

The advantages of sales forecasts go far beyond simply establishing your sales team’s confidence level. Done properly, forecasts can help you and your leadership team set ambitious but achievable sales objectives in relation to broader strategic goals.

As a result, you can create more accurate budgets across the business and better allocate resources to ensure you’ll meet those objectives. In addition, sales forecasts often reveal strategic and operational risks before they become crises.

Quantitative vs. qualitative

Generally, two broad models are used for sales forecasting: quantitative and qualitative.

Quantitative forecasting involves gathering numerical data and applying statistical methods to generate revenue estimates. This usually starts with looking at historical sales results and identifying past trends. You can, for example, break down sales data by time periods, product or service lines, or regions to spot patterns and seasonal fluctuations.

Other internal business metrics also factor into quantitative forecasting. These may include:

Return on investment of marketing campaigns,

Measures related to productivity and staffing levels, and

Inventory metrics.

And the data points don’t stop there. Sales forecasts can incorporate additional quantitative information drawn from global, national and local economic indicators; industry and market trends; and consumer behavior.

Qualitative sales forecasting relies less on hard data and more on the input of pertinent parties inside and outside your company. Such parties include your executive leadership team, as well as members of your sales and marketing departments. However, you can also gather qualitative feedback from customer surveys, focus groups and consultants.

Most businesses combine the quantitative and qualitative models to arrive at an optimal sales forecasting process. Start-ups and companies with limited operating histories may need to rely largely on qualitative input.

Best practices

There’s no one-size-fits-all sales forecasting process. The right one depends on your business’s distinctive features, operational requirements and strategic goals. Nonetheless, certain best practices generally apply to all companies. These include:

Defining the time frame. Most businesses generate sales forecasts monthly or quarterly. Newer companies or small businesses may be able to get away with annual sales forecasts because they have less data to work with. As a company grows, however, it will likely need to perform sales forecasts more often.

Choosing data points carefully and consistently. Quantitative sales forecasts generally must measure the same things over time so you can compare, contrast and pick up trends. When using the qualitative model, you may add contributors as necessary and feasible, but be careful about information overload.

Finding the right analytical method. You can crunch the numbers in various ways. Trend analysis, for instance, is suitable for businesses with stable and sizable historical data. Regression analysis can help you understand relationships between variables, such as marketing budget and sales. There are other approaches to consider as well.

Leveraging technology. You may be able to use software you already own to generate sales forecasts. For example, many customer relationship management platforms offer reporting functions that can help with forecasting. There’s also dedicated sales forecasting software available. Artificial intelligence is having a major positive impact on these products.

Continuous improvement

If your company is already generating sales forecasts, give yourself some credit. However, remember that you must continuously improve your current process to refine its accuracy, adapt to changes and incorporate evolving best practices. FMD can help you create a sales forecasting process or improve the one you have in place.

How to Evaluate and Undertake a Business Transformation

Many industries have undergone monumental changes over the last decade or so. Broadly, there are two ways to adapt to the associated challenges: slowly or quickly.

Although there’s much to be said about small, measured responses to economic change, some companies might want to undertake a more urgent, large-scale revision of their operations. This is called a “business transformation” and, under the right circumstances, it can be a prudent move.

Defining the concept

A business transformation is a strategically planned modification of how all or part of a company operates. In its broadest form, a transformation might change the very mission of the business. For example, a financial consulting firm might become a software provider. However, there are other more subtle variations, including:

Digital transformation (implementing new technologies to digitalize every business function),

Operational transformation (streamlining workflows or revising processes to change operations fundamentally), and

Structural transformation (altering the leadership structure or reorganizing departments/units).

The overarching goal of any transformation is to boost the company’s financial performance by increasing efficiencies, improving customer service, seizing greater market share or entering a new market.

Making the call

Choosing to undertake a business transformation of any kind is a major decision. Before making the call, you and your leadership team must evaluate your company’s market position and identify what’s inhibiting growth and possibly even leading toward a downturn. Common indicators that a transformation may be needed include:

Declining revenues with little to no projections of upswings,

Outdated processes that are creating errors and upsetting customers,

Intensifying competition that will be difficult or impossible to counter, and

Shifts in customer expectations or demand that call for substantive changes.

To decide whether a business transformation is appropriate, you must conduct due diligence through measures such as analyzing financial data and market trends, gathering customer feedback, and obtaining the counsel of professional advisors.

5 general steps to follow

So, let’s say you do your due diligence and decide to move forward with a business transformation. Generally, companies follow five steps:

1. Set a clearly worded objective. The more specific you are in describing how you intend to transform your business, the more likely you are to accomplish that objective. Set aside the time and exercise the patience needed to find specificity and consensus with your leadership team, key employees and professional advisors.

2. Forecast the financial, legal and operational impacts. You must paint a realistic picture of how the big change will likely affect the business during and after the transformation. This is another step in which your professional advisors are critical. With their help, generate financial forecasts related to expenses and revenue changes, identify potential compliance risks and so forth.

3. Map out the road ahead. With a clear vision in mind and a wealth of information in hand, create a detailed roadmap to the transformation. A phased approach is typically best. Define milestones and align performance metrics to each phase. In addition, develop contingency plans in case you wander off course.

4. Communicate with stakeholders. Devise a communication strategy that addresses all key stakeholders — including employees, independent contractors, customers, vendors, suppliers, investors and lenders. Tailor the strategy to each audience, promoting transparency and encouraging buy-in.

5. Monitor progress and adapt as necessary. To increase your odds of success, you and your leadership team need to “stay on it.” Track metrics, allocate time to discussing progress, and be ready to overcome internal and external challenges.

Bold move

Business transformations are difficult to achieve. Insufficient planning, lack of financial oversight and employee resistance can derail efforts. Meanwhile, the necessary investments may strain cash flow. Worst of all, if you fail, you’ll have squandered all those resources.