BLOG

4 Ways Business Owners Can Make “The Leadership Connection”

To get the most from any team, its leader must establish a productive rapport with each member. Of course, that’s easier said than done if you own a company with scores or hundreds of workers. Still, it’s critical for business owners to make “the leadership connection” with their employees.

Simply put, the leadership connection is an authentic bond between you and your staff. When it exists, employees feel like they genuinely know you — if not literally, then at least in the sense of having a positive impression of your personality, values and vision. Here are four ways to build and strengthen the leadership connection with your workforce.

1. Listen and share

Today’s employees want more than just equitable compensation and benefits. They want a voice. To that end, set up an old-fashioned suggestion box or perhaps a more contemporary email address or website portal for staff to share concerns and ask questions.

You can directly reply to queries with broad implications. Meanwhile, other executives or managers can handle questions specific to a given department or position. Choose communication channels thoughtfully. For example, you might share answers through company-wide emails or make them a feature of an internal newsletter or blog. Video messages can also be effective.

2. Stage formal get-togethers

Although leaders at every level need to be careful about calling too many meetings, there’s still value in getting everyone together in one place in real time. At least once a year, consider holding a “town hall” meeting where:

The entire company gathers to hear you (and perhaps others) present on the state of the business, and

Anyone can ask a question and have it answered (or receive a promise for an answer soon).

Town hall meetings are a good venue for discussing the company’s financial performance and establishing expectations for the immediate future.

You could even take it to the next level by organizing a company retreat. One of these events may not be feasible for businesses with bigger workforces. However, many small businesses organize off-site retreats so everyone can get better acquainted and explore strategic ideas.

3. Make appearances

Meetings are useful, but they shouldn’t be the only time staff see you. Interact with them in other ways as well. Make regular visits to each unit, department or facility of your business. Give managers a chance to speak with you candidly. Sit in on meetings; ask and answer questions.

By doing so, you may gather ideas for eliminating costly redundancies and inefficiencies. Maybe you’ll even find inspiration for your next big strategic move. Best of all, employees will likely get a morale boost from seeing you take an active interest in their corners of the company.

4. Have fun and celebrate

All work and no play makes business owners look dull and distant. Remember, employees want to get to know you as a person, at least a little bit. Show positivity and a sense of humor. Share appropriate personal interests, such as sports or caring for pets, in measured amounts.

Above all, don’t neglect to celebrate your business’s successes. Be enthusiastic about hitting sales numbers or achieving growth targets. Recognize the achievements of others — not just on the executive team but throughout the company. Give shout-outs to staff members on their birthdays and work anniversaries.

It’s all about trust

At the end of the day, the leadership connection is all about building trust. The greater your employees’ trust in you, the more loyal, engaged and productive they’ll likely be. FMD can help you measure your business’s productivity and evaluate workforce development costs.

Cost Management is Critical for Companies Today

Many business owners take an informal approach to controlling costs, tackling the issue only when it becomes an obvious problem. A better way to handle it is through proactive, systematic cost management. This means segmenting your company into its major spending areas and continuously adjusting how you allocate dollars to each. Here are a few examples.

Supply chain

Most supply chains contain opportunities to control costs better. Analyze your company’s sourcing, production and distribution methods to find them. Possibilities include:

Renegotiating terms with current suppliers,

Finding new suppliers, particularly local ones, and negotiating better deals, and

Investing in better technology to reduce wasteful spending and overstocking.

If you haven’t already, openly address what’s on everyone’s mind these days: global tariffs. Work with your leadership team and professional advisors to study how current tariffs affect your company. In addition, do some scenario planning to anticipate what you should do if those tariffs rise or fall.

Product or service portfolio

You might associate the word “portfolio” with investments. However, every business has a portfolio of products and services that it sells to customers. Review yours regularly. Like an investment portfolio, a diversified product or service portfolio may better withstand market risks. But offering too many products or services exhausts resources and exposes you to high costs.

Consider simplifying your portfolio to eliminate the costs of underperforming products or services. Of course, you should do so only after carefully analyzing each offering’s profitability. Focusing on only high-margin or in-demand products or services can reduce expenses, increase revenue and strengthen your brand.

Operations

Many business owners are surprised to learn that their companies’ operations cost them money unnecessarily. This is often the case with companies that have been in business for a long time and gotten used to doing things a certain way.

The truth is, “we’ve always done it that way” is usually a red flag for inefficiency or obsolescence. Undertake periodic operational reviews to identify bottlenecks, outdated processes and old technology. You may lower costs, or at least control them better, by upgrading equipment, implementing digital workflow solutions or “rightsizing” your workforce.

Customer service

Customer service is the “secret sauce” of many small to midsize companies, so spending cuts here can be risky. But you still need to manage costs proactively. Relatively inexpensive technology — such as website-based knowledge centers, self-service portals and chatbots — may reduce labor costs.

Perform a comprehensive review of all your customer-service channels. You may be overinvesting in one or more that most customers don’t value. Determine where you’re most successful and focus on leveraging your dollars there.

Marketing and sales

These are two other areas where you want to optimize spending, not necessarily slash it. After all, they’re both critical revenue drivers. When it comes to marketing, you might be able to save dollars by:

Refining your target audience to reduce wasted “ad spend,”

Embracing lower-cost digital strategies, and

Analyzing customer data to personalize outreach.

Data is indeed key. If you haven’t already, strongly consider implementing a customer relationship management (CRM) system to gather, organize and analyze customer and prospect info. In the event you’ve had the same CRM system for a long time, look into whether an upgrade is in order.

Regarding sales costs, reevaluate your compensation methods. Can you adjust commissions or incentives to your company’s advantage without disenfranchising sales staff? Also, review travel budgets. Now that most salespeople are back on the road, their expenses may rise out of proportion with their results. Virtual meetings can reduce travel expenses without sacrificing engagement with customers and prospects.

The struggle is real

Cost management isn’t easy. Earlier this year, a Boston Consulting Group study found that, on average, only 48% of cost-saving targets were achieved last year by the 570 C-suite executives surveyed. Beating that percentage will take some work. To that end, please contact FMD. We can analyze your spending and provide guidance tailored to your company’s distinctive features.

EBHRAs: A Flexible Health Benefits Choice for Businesses

Today’s companies have several kinds of tax-advantaged accounts or arrangements they can sponsor to help employees pay eligible medical expenses. One of them is a Health Reimbursement Arrangement (HRA).

Under an HRA, your business sets up and wholly funds a plan that reimburses participants for qualified medical expenses of your choosing. (To be clear, employees can’t contribute.) The primary advantage is that plan design is very flexible, giving you greater control of your “total benefits spend.” Plus, your company’s contributions are tax deductible.

How flexible are HRAs? They’re so flexible that businesses have multiple plan types to choose from. Let’s focus on one in particular: excepted benefit HRAs (EBHRAs).

4 key rules

Although traditional HRAs integrated with group health insurance provide significant control, they’re still subject to mandates under the Public Health Service Act (PHSA), which was amended by the Affordable Care Act (ACA). This means you must deal with prohibitions on annual and lifetime limits for essential health benefits and requirements to provide certain preventive services without cost-sharing.

Because employer contributions to EBHRAs are so limited, participants’ accounts under these plans qualify as “excepted benefits.” Therefore, these plans aren’t subject to the ACA’s PHSA mandates. Any size business may sponsor an EBHRA, but you must follow certain rules. Four of the most important are:

1. Contribution limits. In 2025, employer-sponsors may contribute up to $2,150 to each participant per plan year. You can, however, choose to contribute less. You can also decide whether to allow carryovers from year to year, which don’t count toward the annual limit.

2. Qualified reimbursements. An EBHRA may reimburse any qualified, out-of-pocket medical expense other than premiums for:

Individual health coverage,

Medicare, and

Non-COBRA group coverage.

Premiums for coverage consisting solely of excepted benefits can be reimbursed, as can premiums for short-term, limited-duration insurance (STLDI). However, under certain circumstances, federal agencies may prohibit small employer EBHRAs in some states from allowing STLDI premium reimbursement. (Contact your benefits advisor for further information.)

3. Required other coverage. Employer-sponsors must make other non-excepted, non-account-based group health plan coverage available to EBHRA participants for the plan year. Thus, you can’t also offer a traditional HRA.

4. Uniform availability. An EBHRA must be made available to all similarly situated individuals under the same terms and conditions, as defined and provided by applicable regulations.

Additional compliance matters

An EBHRA’s status as an excepted benefit means it’s not subject to the ACA’s PHSA mandates (as mentioned) or the portability and nondiscrimination rules of the Health Insurance Portability and Accountability Act (HIPAA).

However, EBHRAs are subject to HIPAA’s administrative simplification requirements. This includes the law’s privacy and security rules unless an exception applies — such as for certain small self-insured, self-administered plans.

In addition, like traditional HRAs integrated with group health insurance, EBHRAs sponsored by businesses are generally subject to the Employee Retirement Income Security Act (ERISA). This means:

Reimbursement requests must comply with ERISA’s claim and appeal procedures,

Participants must receive a summary plan description, and

Other ERISA requirements may apply.

Finally, EBHRAs must comply with ERISA’s nondiscrimination rules. These ensure that benefits provided under the plan don’t disproportionately favor highly compensated employees over non-highly compensated ones.

Many factors to analyze

As noted above, the EBHRA is only one type of plan your company can consider. Others include traditional HRAs integrated with group health insurance, qualified small employer HRAs and individual coverage HRAs.

Choosing among them — or whether to sponsor an HRA at all — will call for analyzing factors such as what health benefits you already offer, which employees you want to cover, how much you’re able to contribute and which medical expenses you wish to reimburse. Let FMD help you evaluate all your benefit costs and develop a strategy for health coverage that makes the most sense for your business.

How Companies Can Spot Dangers by Examining Concentration

At first glance, the word “concentration” might seem to describe a positive quality for any business owner. You need to concentrate, right? Only through laser focus on the right strategic goals can your company reach that next level of success.

In a business context, however, concentration can refer to various aspects of your company’s operations. And examining different types of it may help you spot certain dangers.

Evaluate your customers

Let’s start with customer concentration, which is the percentage of revenue generated from each customer. Many small to midsize companies rely on only a few customers to generate most of their revenue. This is a precarious position to be in.

The dilemma is more prevalent in some industries than others. For example, a retail business will likely market itself to a relatively broad market and generally not face too much risk related to customer concentration. A commercial construction company, however, may serve only a limited number of clients that build, renovate or maintain offices or other facilities.

How do you know whether you’re at risk? One rule of thumb says that if your biggest five customers make up 25% or more of your revenue, your customer concentration is generally high. Another simple measure says that, if any one customer represents 10% or more of revenue, you’re at risk of having elevated customer concentration.

In an increasingly specialized world, many businesses focus solely on specific market segments. If yours is one of them, you may not be able to do much about customer concentration. In fact, the very strength of your company could be its knowledge and attentiveness to a limited number of buyers.

Nonetheless, know your risk and explore strategic planning concepts that may help you mitigate it. If diversifying your customer base isn’t an option, be sure to maintain the highest level of service.

Look at other areas

There are other types of concentration. For instance, vendor concentration refers to the number and types of vendors a company uses to support its operations. Relying on too few vendors is risky. If any one of them goes out of business or substantially raises prices, the company could suffer a severe rise in expenses or even find itself unable to operate.

Your business may also be affected by geographic concentration. This is how a physical location affects your operations. For instance, if your customer base is concentrated in one area, a dip in the regional economy or the arrival of a disruptive competitor could negatively impact profitability. Small local businesses are, by definition, subject to geographic concentration. However, they can still monitor the risk and explore ways to mitigate it — such as through online sales in the case of retail businesses.

You can also look at geographic concentration globally. Say your company relies solely or largely on a specific foreign supplier for iron, steel or other materials. That’s a risk. Tariffs, which have been in the news extensively this year, can significantly impact your costs. Geopolitical and environmental factors might also come into play.

Third, stay cognizant of your investment concentration. This is how you allocate funds toward capital improvements, such as better facilities, machinery, equipment, technology and talent. The term can also refer to how your company manages its investment portfolio, if it has one. Regularly reevaluate risk tolerance and balance. For instance, are you overinvesting in technology while underinvesting in hiring or training?

Study your company

As you can see, concentration takes many different forms. This may explain why business owners often get caught off guard by the sudden realization that their companies are over- or under-concentrated in a given area. FMD can help you perform a comprehensive risk assessment that includes, among other things, developing detailed financial reports highlighting areas of concentration.

Mitigate the Risks: Tips for Dealing with Tariff-Driven Turbulence

President Trump’s “Liberation Day” announcement of global tariffs caught businesses, as well as foreign countries and worldwide financial markets, off guard. While the president has long endorsed the imposition of tariffs, many businesses expected him to take a targeted approach. Instead, Trump rolled out a baseline tariff on all imports to the United States and higher tariffs on certain countries, including some of the largest U.S. trading partners. (On April 9, Trump announced a 90-day pause on some reciprocal tariffs, with a 10% baseline tariff remaining in effect for most countries and a 145% tariff on imports from China.)

The tariff plan sent businesses, both large and small, scrambling. Even companies accustomed to dealing with tariffs have been shaken because this round is so much more extensive and seemingly subject to change than those in the past.

Proponents of tariffs say they can be used as a negotiating tool to get other countries to lower their tariffs on U.S. imports, thereby leveling the global trade playing field. They also argue that if domestic and foreign companies relocate to the United States, it’ll create jobs for Americans, fuel construction industry growth and provide additional tax revenue.

Since more changes are expected as countries and industries negotiate with the administration for reduced rates and exemptions, some degree of uncertainty is likely to prevail for at least the short term. In the meantime, businesses have several areas they should focus on to reduce the tariff hit to their bottom lines.

1. Financial forecasting

No business should decide how to address tariff repercussions until they’ve conducted a comprehensive financial analysis to understand how U.S. and retaliatory tariffs will affect costs. You might find, for example, that your business needs to postpone impending plans for capital asset purchases or expansion.

Modeling, or scenario planning, is often helpful during unpredictable periods. Begin by identifying all the countries involved in your supply chain, whether you deal with them directly or through your suppliers, and the applicable tariffs, whether you’re importing or exporting goods.

You can then develop a model that projects how different sourcing scenarios might play out. The model should compare not only the costs of foreign vs. domestic options but also the resulting impact on your pricing, labor costs, cash flow and, ultimately, profitability. This information can allow you to build contingency plans to help reduce the odds of being caught flat-footed as new developments unfurl.

Modeling can provide valuable guidance if you’re considering reshoring your operations. Of course, reshoring isn’t a small endeavor. Moreover, U.S. infrastructure may not be adequate for your business needs.

Manufacturers also should note the shortage of domestic manufacturing workers. According to pre-tariff analysis from the National Association of Manufacturers, the U.S. manufacturing industry could require some 3.8 million jobs by 2033, and more than 1.9 million may go unfilled.

2. Pricing

Perhaps the most obvious tactic for companies incurring higher costs due to tariffs is to pass the increases along to their customers. It’s not that simple, though.

Before you raise your prices, you must take into account factors such as your competitors’ pricing and how higher prices might affect demand. The latter is especially critical for price-sensitive consumer goods where even a small price jump could undermine demand.

Consumers have already been cutting back on spending based on rising fears of inflation and a possible recession. Price increases, therefore, are better thought of as a single component in a more balanced approach.

3. Foreign Trade Zones

You may be able to take advantage of Foreign Trade Zones (FTZs) to minimize your tariff exposure. In these designated areas near U.S. ports of entry, a company can move goods in and out of the country for operations (including assembly, manufacturing and processing) but pay reduced or no tariffs.

Tariffs are paid when the goods are transferred from an FTZ into the United States for consumption. While in the zone, though, goods aren’t subject to tariffs. And, if the goods are exported, no tariff applies.

Note: Trump already has narrowed some of the potential benefits of FTZs, so avoid making them a cornerstone of your tariff strategy.

4. Internal operations

If your company’s suppliers are in high-tariff countries, you can look into switching to lower-cost suppliers in countries that have negotiated lower tariffs.

You may not be able to escape higher costs stemming from tariffs, but you can take steps to cut other costs by streamlining operations. For example, you could invest in technologies to improve efficiency or trim worker hours and employee benefits. You also should try to renegotiate contracts with suppliers and vendors, even if those relationships aren’t affected by tariffs. Such measures might make it less necessary to hike your prices.

You can control your overall costs as well by breaking down departmental silos so the logistics or procurement department isn’t making tariff-related decisions without input from others. Your finance and tax departments need to weigh in to achieve the optimal cost structures.

5. Tax planning

Maximizing your federal and state tax credits is paramount in financially challenging times. Technology investments, for example, may qualify for Section 179 expensing and bonus depreciation (which may return to 100% in the first year under the upcoming tax package being negotiated in Congress). Certain sectors may benefit from the Sec. 45X Advanced Manufacturing Production Credit or the Sec. 48D Advanced Manufacturing Investment Credit. Several states also offer tax credits for job creation, among other tax incentives.

This may be a wise time to consider changing your inventory accounting method, if possible. The last-in, first-out (LIFO) method assumes that you use your most recently purchased materials first. The cost of the newer, pricier items is charged first to the cost of goods sold, boosting it and cutting both your income and taxes. Bear in mind, though, that LIFO isn’t permitted under the International Financial Reporting Standards and is more burdensome than the first-in, first-out method.

6. Compliance

Regardless of the exact percentages of U.S. and retaliatory tariffs, you can count on tighter scrutiny of your compliance with the associated rules and requirements. These probably will become more complicated than they’ve been in the past.

For example, expect greater documentation requirements and shifting rules for identifying an item’s country of origin. The higher compliance burden alone will ramp up your costs — but the costs of noncompliance could be far greater.

Stay vigilant

The tariff landscape is rapidly evolving. You need to monitor the actions by the Trump administration, the responses of other countries and how they affect your business operations. You may have to pivot as needed to keep costs low (by reshoring or switching to suppliers in low-tariff countries). If you don’t have the requisite financial expertise on staff to keep up with it all, we can help. Contact FMD today about how to plan ahead — and stay ahead of the changes.

Businesses Considering Incorporation should Beware of the Reasonable Compensation Conundrum

Small to midsize businesses have valid reasons for incorporating, not the least of which is putting that cool “Inc.” at the end of their names. Other reasons include separating owners’ personal assets from their business liabilities and offering stock options as an employee incentive.

If you’re considering incorporation for your company, however, it’s essential to be aware of the associated risks. One of them is the reasonable compensation conundrum.

How much is too much?

Let’s say you decide to convert your business to a C corporation. After completing the incorporation process, you can pay owners, executives and other highly compensated employees some combination of compensation and dividends.

More than likely, you’ll want to pay your highly compensated employees more in compensation and less in dividends because compensation is tax deductible and dividends aren’t. But be careful — the IRS may be watching. If it believes you’re excessively compensating a highly compensated employee for tax avoidance purposes, it may challenge your compensation approach.

Such challenges typically begin with an audit and may result in the IRS being allowed to reclassify compensation as dividends — with penalties and interest potentially tacked on. What’s worse, if the tax agency succeeds with its challenge, the difference between what you paid a highly compensated employee and what the tax agency considers a reasonable amount for the services rendered usually isn’t deductible.

Of course, you can contest an IRS challenge. However, doing so usually involves considerable legal expenses and time — and a positive outcome is far from guaranteed.

Note: S corporations are a different story. Under this entity type, income and losses usually “pass through” to business owners at the individual level and aren’t subject to payroll tax. Thus, S corporation owners usually prefer to receive distributions. As a result, the IRS may raise a reasonable compensation challenge when it believes a company’s owners receive too little salary.

What are the factors?

There’s no definitive bright-line test for determining reasonable compensation. However, over the years, courts have considered various factors, including:

The nature, extent and scope of an employee’s work,

The employee’s qualifications and experience,

The size and complexity of the business,

A comparison of salaries paid to the sales, gross income and net worth of the business,

General economic conditions,

The company’s financial status,

The business’s salary policy for all employees,

Salaries of similar positions at comparable companies, and

Historical compensation of the position.

It’s also important to assess whether the business and employee are dealing at an “arm’s length,” and whether the employee has guaranteed the company’s debts.

Can you give me an example?

Just a few years ago, a case played out in the U.S. Tax Court illustrating the risks of an IRS challenge regarding reasonable compensation.

The owner of a construction business structured as a C corporation led his company through tough times and turned it into a profitable enterprise. When the business recorded large profits in 2015 and 2016, primarily because of the owner’s personal efforts and contacts, it paid him a bonus of $5 million each year in addition to his six-figure salary. The IRS claimed this was excessive.

The Tax Court relied heavily on expert witnesses to make its determination. Ultimately, it decided against the business, finding that reasonable amounts for the bonuses were $1.36 million in 2015 and $3.68 million in 2016, respectively. (TC Memo 2022-15)

Who can help?

As your business grows, incorporation may help your company guard against certain risks and achieve a greater sense of stature. However, there are tax complexities to consider. If you’re thinking about it, please contact FMD for help identifying the advantages and risks from both tax and strategic perspectives.

Is Your Business on Top of its Tech Stack?

Like many business owners, you’ve probably received a lot of technology advice. One term you may hear frequently is “tech stack.” Information technology (IT) folks love to throw this one around while sharing their bits and bytes of digital wisdom.

Well, they’re not wrong about its importance. Your tech stack is crucial to maintaining smooth operations, but it can be a major drain on cash flow if not managed carefully.

Everything you use

For the purpose of running a business, a tech stack can be defined as all the software and other digital tools used to support the company’s operations and IT infrastructure. It includes assets such as your:

Accounting software,

Customer relationship management platform,

Project management tools,

Cloud storage, and

Communication apps.

Note: In a purely IT context, the term is widely defined as the set of technologies used to develop an application or website.

For businesses, a tech stack’s objective is to streamline workflows and promote productivity while maintaining strong cybersecurity. Unfortunately, as it grows, a tech stack can leave companies struggling with overspending, inefficiencies and employee apathy.

Case in point: For its 2025 State of Digital Adoption Report, software platform provider WalkMe surveyed nearly 4,000 enterprise leaders and employees worldwide. The data showed that about 43% of enterprise tech stacks are currently more complex than they were three years ago. Disturbingly, the report found the average large enterprise lost $104 million in 2024 because of underused technology, fragmented IT strategy and low employee adoption of tech tools.

Although these results focus on larger companies, small to midsize businesses face the same risks. Over time, companies often layer technologies upon technologies, sometimes introducing redundant or extraneous tools that are largely ignored.

5 factors to consider

Balancing functionality and innovation without overspending is the key to staying on top of your tech stack. Here are five factors to focus on:

1. Composition. Many business owners lose track of the many complex elements of their tech stacks. The best way to stay informed is to conduct regular IT audits. These are formal, systematic reviews of your IT infrastructure, which includes your tech stack. Audits often reveal redundant software subscriptions and underused or forgotten software licenses.

2. Integration/compatibility. When tech tools don’t play well together — or at all — data silos spring up and redundant work drags everyone down. This leads to more errors and less productivity. When managing your tech stack, choose solutions that integrate well across your operations. As feasible, replace those that don’t.

3. Price to value. Choosing IT tools primarily based on cost is risky. Although you should budget carefully, opting for cheaper solutions can ultimately increase technology expenses because of greater inefficiencies and the constant need to add tools to fill functionality gaps. Stay mindful of getting good value for the price and make choices that align with your strategic objectives.

4. Scalability. Generally, as a business grows, its technology needs expand and evolve. That doesn’t mean you always have to buy new software, however. Look for solutions that can scale up with growth or down during slower periods. Shop for assets that offer flexibility along with the right functionality.

5. Adoptability. Your company could have the most powerful software tool in existence, but if it sits unused, that item is just a wasted expense taking up space in your tech stack. Add new technology cautiously. Consult your leadership team, survey the employees who’ll be using it and ask for vendor references. When you do buy something, roll it out with an effective communication strategy and thorough training.

A technological tree

Like a tree, a tech stack can grow out of control and become a nuisance or even a danger to everyone around it. Properly pruned and otherwise well-maintained, however, it can be a powerful and functional business feature. Let FMD help you identify all your technology costs and assess the return on investment of every component of your tech stack.

How Companies Can Better Control IT Costs

Most small to midsize businesses today are constantly under pressure to upgrade their information technology (IT). Whether it’s new software, a better way to use the cloud or a means to strengthen cybersecurity, there’s always something to spend more money on.

If your company keeps blowing its IT budget, rest assured — you’re not alone. The good news is that you and your leadership team may be able to control these costs better through various proactive measures.

Set a philosophy and exercise governance

Assuming your company hasn’t already, establish a coherent IT philosophy. Depending on its industry and mission, your business may need to spend relatively aggressively on technology to keep up with competitors. Or maybe it doesn’t. You could decide to follow a more cautious spending approach until these costs are under control.

Once you’ve set your philosophy, develop clear IT governance policies and procedures for purchases, upgrades and usage. These should, for example, mandate and establish approval workflows and budgetary oversight. You want to ensure that every dollar spent aligns with current strategic objectives and will likely result in a positive return on investment (ROI).

Beware of shiny new toys! Many businesses exceed their IT budgets when one or two decision-makers can’t control their enthusiasm for the latest and greatest solutions. Grant final approval for major purchases, or even a series of minor ones, only after carefully analyzing the technology you have in place and identifying legitimate gaps or shortcomings.

Also, remember that overspending on technology is often driven by undertrained employees. Teach and remind your users to adhere to your IT policies and follow procedures. Doing so can help prevent costly operational mistakes and cybersecurity breaches.

Conduct regular audits

You can’t control costs in any business area unless you know precisely what they are. To get the information you need, regularly conduct IT audits. These are formal, systematic reviews of your IT infrastructure, policies, procedures and usage. IT audits often reveal budget drainers such as:

Redundant subscriptions for software or other tech services,

Underused or forgotten software licenses, and

Outdated or abandoned hardware.

You may discover, for instance, that you’re paying for several different software products with overlapping functionalities. Choosing one and discarding the others could generate substantial savings.

As you search for overspending, also look for examples of IT expenditures delivering a good ROI. You want to be able to refine and repeat whatever decision-making process led you to those wins.

Keep an eye on the cloud

One specific type of IT expense that plagues many businesses relates to cloud services. Like many companies, yours probably uses a “pay as you go” subscription model that includes discounts or rate reductions for lower usage. However, if you don’t monitor your actual cloud usage and claim those discounts or cheaper rates, you can wind up overpaying for months or even years without realizing it.

To avoid this sad fate, ensure that at least one person within your business is well-acquainted with your cloud services contract. Assign this individual (usually a technology executive) the responsibility of making sure the company claims all discounts or rate adjustments it’s entitled to.

One best practice to strongly consider is setting up weekly cloud cost reports that go to the leadership team. Also, be prepared to occasionally renegotiate your cloud services contract so it’s as straightforward as possible and optimally suited to your business’s needs.

Don’t give up

To be clear, controlling IT costs should never mean cutting corners or scrimping on mission-critical technology expenses — particularly those related to cybersecurity. That said, you also should never give up on managing your IT budget. FMD can help you develop a tailored cost-control strategy that keeps your technology current and supports your business objectives.

Growing the Business Means Supporting your Managers

Many different shortcomings can hold back the growth of a company. Some are obvious, such as poor cash flow management or flawed strategic plans. Others aren’t so easy to see.

Take, for example, disjointed or under-supported managers. If you don’t dedicate the time and resources to strengthening the bonds of your management team, and provide the support they need, your company may struggle with slower growth as a consequence.

Follow a collaborative approach

A good place to start is by making sure you’re following a collaborative approach to running the business. Develop strategic goals with your management team’s input and buy-in so everyone is pulling in the same direction. From there, actively work to keep managers engaged in meeting department-specific objectives related to strategic goals.

Collaboration has other benefits, too. More individuals participating in decision-making can mean more creative and well-thought-out solutions. A collaborative approach also distributes the burden of strategic planning so it doesn’t fall on only your shoulders. Sharing responsibility for key decisions — particularly as a business grows — is vital to facilitating progress and seizing opportunities.

Build an accessible knowledge base

Involving managers in decision-making calls for developing a robust, accessible knowledge base about your company’s product or service lines, organizational structure, market, customer base and operating environment. Your management team must be able to view, in real time, the information they need to contribute to strategic planning and guide their departments.

The good news is that today’s technology allows you to create a centralized platform for authorized users to share and access critical data so everyone is on the same page. For example, you can use enterprise resource planning software to gather, store and analyze business intelligence related to core processes such as human resources, financial management and reporting, and supply chain management. You can integrate customer relationship management software to track and share data related to customers, prospects and key contacts.

When in doubt, conduct an assessment

If you’re unsure where your management team stands, you may want to perform a formal assessment. This entails undertaking a thorough and confidential review of every manager to identify issues — whether cultural, technical or interpersonal — that may be detracting from team performance.

To help ensure objectivity, many businesses engage outside consultants specializing in executive or leadership development to perform such assessments. The assessments generally consist of live or virtual interviews, sometimes in group settings, and written or online evaluations. The goal is to gain insights into:

Individual and group strengths and weaknesses,

Team dynamics,

Barriers to success,

Areas of improvement, and

Untapped opportunities.

Assessment providers typically issue results in written reports and debriefing sessions. Most will help you create an action plan to make use of the information gathered.

Consider an annual retreat

To take management team building to the next level, you may want to hold annual retreats. Doing so can be particularly important following one of the aforementioned assessments.

Management retreats typically follow a more intense format than company-wide team-building events. Ways to structure each retreat are limited only by budget, creativity and perhaps team members’ physical limitations. The goal is to break down functional silos and communication barriers and build up a greater sense of trust and unity.

However, to fully realize the potential value of a retreat, you must follow up. That means harnessing the experiences and breakthroughs that occur during the event and using them to create an action plan for improving management performance back at the office. (If you’ve also conducted a management team assessment, you can combine the two action plans.)

Give them support

It’s all too easy for managers to get caught up in their respective departments’ day-to-day trials and travails. That’s how growth inhibitors such as knowledge silos and leadership conflicts happen. Give your management team the encouragement and support it deserves. FMD can help you identify and analyze all the costs of performance development at every level of your business.

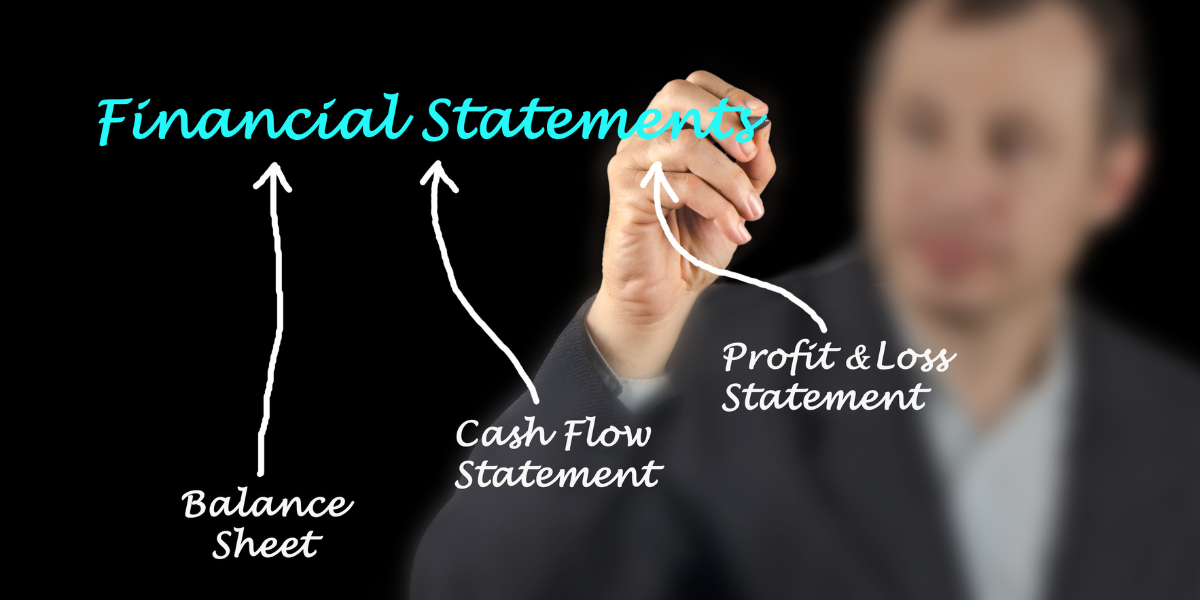

Business Owners Should Get Comfortable with their Financial Statements

Financial statements can fascinate accountants, investors and lenders. However, for business owners, they may not be real page-turners.

The truth is each of the three parts of your financial statements is a valuable tool that can guide you toward reasonable, beneficial business decisions. For this reason, it’s important to get comfortable with their respective purposes.

The balance sheet

The primary purpose of the balance sheet is to tally your assets, liabilities and net worth, thereby creating a snapshot of your business’s financial health during the statement period.

Net worth (or owners’ equity) is particularly critical. It’s defined as the extent to which assets exceed liabilities. Because the balance sheet must balance, assets need to equal liabilities plus net worth. If the value of your company’s liabilities exceeds the value of its assets, net worth will be negative.

In terms of operations, just a couple of balance sheet ratios worth monitoring, among many, are:

Growth in accounts receivable compared with growth in sales. If outstanding receivables grow faster than the rate at which sales increase, customers may be taking longer to pay. They may be facing financial trouble or growing dissatisfied with your products or services.

Inventory growth vs. sales growth. If your business maintains inventory, watch it closely. When inventory levels increase faster than sales, the company produces or stocks products faster than they’re being sold. This can tie up cash. Moreover, the longer inventory remains unsold, the greater the likelihood it will become obsolete.

Growing companies often must invest in inventory and allow for increases in accounts receivable, so upswings in these areas don’t always signal problems. However, jumps in inventory or receivables should typically correlate with rising sales.

Income statement

The purpose of the income statement is to assess profitability, revenue generation and operational efficiency. It shows sales, expenses, and the income or profits earned after expenses during the statement period.

One term that’s commonly associated with the income statement is “gross profit,” or the income earned after subtracting cost of goods sold (COGS) from revenue. COGS includes the cost of labor and materials required to make a product or provide a service. Another important term is “net income,” which is the income remaining after all expenses — including taxes — have been paid.

The income statement can also reveal potential problems. It may show a decline in gross profits, which, among other things, could mean production expenses are rising more quickly than sales. It may also indicate excessive interest expenses, which could mean the business is carrying too much debt.

Statement of cash flows

The purpose of the statement of cash flows is to track all the sources (inflows) and recipients (outflows) of your company’s cash. For example, along with inflows from selling its products or services, your business may have inflows from borrowing money or selling stock. Meanwhile, it undoubtedly has outflows from paying expenses, and perhaps from repaying debt or investing in capital equipment.

Although the statement of cash flows may seem similar to the income statement, its focus is solely on cash. For instance, a product sale might appear on the income statement even though the customer won’t pay for it for another month. But the money from the sale won’t appear as a cash inflow until it’s collected.

By analyzing your statement of cash flows, you can assess your company’s ability to meet its short-term obligations and manage its liquidity. Perhaps most importantly, you can differentiate profit from cash flow. A business can be profitable on paper but still encounter cash flow issues that leave it unable to pay its bills or even continue operating.

Critical insights

You can probably find more exciting things to read than your financial statements. However, you won’t likely find anything more insightful regarding how your company is performing financially. FMD can help you not only generate best-in-class financial statements, but also glean the most valuable information from them.

Family Business Focus: Taking it to The Next Level

Family businesses often start out small, with casual operational approaches. However, informal (or nonexistent) policies and procedures can become problematic as such companies grow.

Employees may grumble about unclear, inconsistent rules. Lenders and investors might frown on suboptimal accounting practices. Perhaps worst of all, customers can become disenfranchised by slow or unsatisfying service. Simply put, there may come a time when you have to take it to the next level.

4 critical areas

Has your family-owned company reached the point where it needs to expand its operational infrastructure to handle a larger customer base, manage higher revenue volumes and capitalize on new market opportunities? If so, look to strengthen these four critical areas:

1. Performance management. Family business owners often get used to putting out fires and tying up loose ends. However, as the company grows, doing so can get increasingly difficult and frustrating. Sound familiar? The problem may not lie entirely with your employees. If you haven’t already done so, write formal job descriptions. Then, provide proper training to teach staff members how to fulfill the stated duties.

From there, implement a formal performance management system to evaluate employees, give constructive feedback, and help determine promotions and pay raises. Effective performance management not only helps employees improve, but also contributes to motivation and retention. It’s particularly important for nonfamily staff, who may feel like they’re not being evaluated the same way as working family members.

In addition, if you don’t yet have an employee handbook, write one. Work with a qualified employment attorney to refine the language and ask everyone to sign an acknowledgment that they received and read it.

2. Business processes. Think of your business processes as the pistons of the engine that drives your family-owned company. We’re talking about things such as:

Production of goods or services,

Sales and marketing,

Customer support,

Accounting and financial management, and

Human resources.

The more you document and enhance these and other processes, the easier it is to train staff and improve their performances. Bear in mind that enhancing business processes usually involves streamlining them to reduce manual effort and redundancies.

3. Strategic planning. Many family business owners keep their company visions to themselves. If they do share them, it’s impromptu, around the dinner table or during family gatherings.

As your company grows, formalize your approach to strategic planning. This starts with building a solid leadership team with whom you can share your thoughts and listen to their opinions and ideas. From there, hold regular strategic-planning meetings and perhaps even an annual retreat.

When ready, share company goals with employees and ask for their feedback. Keeping staff in the loop empowers them and helps ensure they buy into the direction you’re taking.

4. Information technology. Nowadays, the systems and software your family business uses to operate can make or break its success. As your company grows, outdated or unscalable solutions will likely inhibit efficiency, undercut competitiveness, and expose you to fraud or hackers.

Running a professional, process-oriented business generally requires integration. This means all your various systems and software should work together seamlessly. You want your authorized users to be able to get to information quickly and easily. You also want to automate as many processes as possible to improve efficiency and productivity.

Last but certainly not least, you must address cybersecurity. Growing family businesses are prime targets for criminals looking to steal data or abduct it for ransom. Internal fraud is an ever-present threat as well.

Change and adapt

Perhaps the most dangerous thing any family business owner can say is, “But we’ve always done it that way!” A growing company is a testament to your hard work, but you’ll need to be adaptable and willing to change to keep it moving forward. FMD can help you reevaluate and improve all your business processes related to accounting, financial management and tax planning.

Weighing the Pluses and Minuses of HDHPs + HSAs for Businesses

Will your company be ready to add a health insurance plan for next year, or change its current one? If so, now might be a good time to consider your options. These things take time.

A popular benefits model for many small to midsize businesses is sponsoring a high-deductible health plan (HDHP) accompanied by employee Health Savings Accounts (HSAs). Like any such strategy, however, this one has its pluses and minuses.

Ground rules

HSAs are participant-owned, tax-advantaged accounts that accumulate funds for eligible medical expenses. To own an HSA, participants must be enrolled in an HDHP, have no other health insurance and not qualify for Medicare.

In 2025, an HDHP is defined as a plan with at least a $1,650 deductible for self-only coverage or $3,300 for family coverage. Also in 2025, participants can contribute pretax income of up to $4,300 for self-only coverage or $8,550 for family coverage. (These amounts are inflation-adjusted annually, so they’ll likely change for 2026.) Those age 55 or older can make additional catch-up contributions of $1,000.

Companies may choose to make tax-deductible contributions to employees’ HSAs. However, the aforementioned limits still apply to combined participant and employer contributions.

Participants can make tax-free HSA withdrawals to cover qualified out-of-pocket medical expenses, such as physician and dentist visits. They may also use their account funds for copays and deductibles, though not to pay many types of insurance premiums.

Pluses to ponder

For businesses, the “HDHP + HSAs” model offers several pluses. First, HDHPs generally have lower premiums than other health insurance plans — making them more cost-effective. Plus, as mentioned, your contributions to participants’ HSAs are tax deductible if you choose to make them. And, overall, sponsoring health insurance can strengthen your fringe benefits package.

HSAs also have pluses for participants that can help you “sell” the model when rolling it out. These include:

Participants can lower their taxable income by making pretax contributions through payroll deductions,

HSAs can include an investment component that may include mutual funds, stocks and bonds,

Account earnings accumulate tax-free,

Withdrawals for qualified medical expenses aren’t subject to tax, and the list of eligible expenses is extensive,

HSA funds roll over from year to year (unlike Flexible Spending Account funds), and

HSAs are portable; participants maintain ownership and control of their accounts if they change jobs or even during retirement.

In fact, HSAs are sometimes referred to as “medical IRAs” because these potentially valuable accounts are helpful for retirement planning and have estate planning implications as well.

Minuses to mind

The HDHP + HSAs model has its minuses, too. Some employees may strongly object to the “high deductible” aspect of HDHPs.

Also, if not trained thoroughly, participants can misuse their accounts. Funds used for nonqualified expenses are subject to income taxes. Moreover, the IRS will add a 20% penalty if an account holder is younger than 65. After age 65, participants can withdraw funds for any reason without penalty, though withdrawals for nonqualified expenses will be taxed as ordinary income.

Expenses are another potential concern. HSA providers (typically banks and investment firms) may charge monthly maintenance fees, transaction fees and investment fees (for accounts with an investment component). Many companies cover these fees under their benefits package to enhance the appeal of HSAs to employees.

Finally, HSAs can have unexpected tax consequences for account beneficiaries. Generally, if a participant dies, account funds pass tax-free to a spouse beneficiary. However, for other types of beneficiaries, account funds will be considered income and immediately subject to taxation.

Powerful savings vehicle

The HDHP + HSAs model helps businesses manage insurance costs, shifts more of medical expense management to participants, and creates a powerful savings vehicle that may attract job candidates and retain employees. But that doesn’t mean it’s right for every company. Please contact FMD for help assessing its feasibility, as well as identifying the cost and tax impact.

ESOPs can Help Business Owners with Succession Planning

Devising and executing the right succession plan is challenging for most business owners. In worst-case scenarios, succession planning is left to chance until the last minute. Chaos, or at least much confusion and uncertainty, often follows.

The most foolproof way to make succession planning easier is to give yourself plenty of time to develop a plan that suits the intricacies of your situation and then gradually implement it. One vehicle that can help “slow your roll” into retirement or whatever your next stage of life may be is an employee stock ownership plan (ESOP).

Little by little

An ESOP is a type of qualified retirement plan that invests solely or mainly in your company’s stock. Because it’s qualified, an ESOP comes with tax advantages as long as you follow the federally enforced rules. These include requirements related to minimum coverage and contribution limits.

Generally, the company sets up an ESOP trust and funds the plan by contributing shares or cash to buy existing shares. Distributions to eligible participants are made in stock or cash. For closely held companies, employees who receive stock have the right to sell it back to the company — exercising “put options” or an “option to sell” — at fair market value during certain time windows.

Although an ESOP involves transferring ownership to employees, it’s different from a management or employee buyout. Unlike a buyout, an ESOP allows owners to cash out and transfer control little by little. During the transfer period, owners’ shares are held in the ESOP trust and voting rights on most issues other than mergers, dissolutions and other major transactions are exercised by the trustees, who may be officers or other company insiders.

Appraisals required

One big difference between ESOPs and other qualified retirement plans, such as 401(k)s, is mandated valuations. The Employee Retirement Income Security Act requires trustees to obtain appraisals by independent valuation professionals to support ESOP transactions. Specifically, an appraisal is needed when the ESOP initially acquires shares from the company’s owners and every year thereafter that the business contributes to the plan.

The fair market value of the sponsoring company’s stock is important because the U.S. Department of Labor specifically prohibits ESOPs from paying more than “adequate consideration” when investing in employer securities. In addition, because employees who receive ESOP shares typically have the right to sell them back to the company at fair market value, the ESOP provides a limited market for its shares.

Drawbacks to consider

An ESOP can play a helpful role in a well-designed succession plan with an appropriately long timeline. However, there are potential drawbacks to consider. You’ll incur costs and considerable responsibilities related to plan administration and compliance. Costs are also associated with annual stock valuations and the need to repurchase stock from employees who exercise put options.

Another potential disadvantage is that ESOPs are available only to corporations of either the C or S variety. Limited liability companies, partnerships and sole proprietorships must convert to one of these two entity types to establish an ESOP. Doing so will raise a variety of tax and financial issues.

In addition, it’s important to explore the potential negative impact of ESOP debt and other expenses on your financial statements and ability to qualify for loans.

Not a no-brainer

ESOPs have become fairly popular among small to midsize businesses. However, the decision to create, launch and administer one is far from a no-brainer. You’ll need to do a deep dive into all the details involved, discuss the concept with your leadership team and get professional advice. Contact FMD for help evaluating whether an ESOP would be a good fit for your business and succession plan.

Embrace the Future: Sales Forecasting for Businesses

So, how are sales looking for next year? It’s not a rhetorical question. Your business should be able to look ahead and accurately estimate how its future sales are shaping up. This practice is called sales forecasting, and doing it well is key to better managing your company’s financial performance.

Why it’s important

Formally defined, sales forecasting is a comprehensive process for estimating future revenue in a given period based on carefully chosen metrics and, often, human input.

The advantages of sales forecasts go far beyond simply establishing your sales team’s confidence level. Done properly, forecasts can help you and your leadership team set ambitious but achievable sales objectives in relation to broader strategic goals.

As a result, you can create more accurate budgets across the business and better allocate resources to ensure you’ll meet those objectives. In addition, sales forecasts often reveal strategic and operational risks before they become crises.

Quantitative vs. qualitative

Generally, two broad models are used for sales forecasting: quantitative and qualitative.

Quantitative forecasting involves gathering numerical data and applying statistical methods to generate revenue estimates. This usually starts with looking at historical sales results and identifying past trends. You can, for example, break down sales data by time periods, product or service lines, or regions to spot patterns and seasonal fluctuations.

Other internal business metrics also factor into quantitative forecasting. These may include:

Return on investment of marketing campaigns,

Measures related to productivity and staffing levels, and

Inventory metrics.

And the data points don’t stop there. Sales forecasts can incorporate additional quantitative information drawn from global, national and local economic indicators; industry and market trends; and consumer behavior.

Qualitative sales forecasting relies less on hard data and more on the input of pertinent parties inside and outside your company. Such parties include your executive leadership team, as well as members of your sales and marketing departments. However, you can also gather qualitative feedback from customer surveys, focus groups and consultants.

Most businesses combine the quantitative and qualitative models to arrive at an optimal sales forecasting process. Start-ups and companies with limited operating histories may need to rely largely on qualitative input.

Best practices

There’s no one-size-fits-all sales forecasting process. The right one depends on your business’s distinctive features, operational requirements and strategic goals. Nonetheless, certain best practices generally apply to all companies. These include:

Defining the time frame. Most businesses generate sales forecasts monthly or quarterly. Newer companies or small businesses may be able to get away with annual sales forecasts because they have less data to work with. As a company grows, however, it will likely need to perform sales forecasts more often.

Choosing data points carefully and consistently. Quantitative sales forecasts generally must measure the same things over time so you can compare, contrast and pick up trends. When using the qualitative model, you may add contributors as necessary and feasible, but be careful about information overload.

Finding the right analytical method. You can crunch the numbers in various ways. Trend analysis, for instance, is suitable for businesses with stable and sizable historical data. Regression analysis can help you understand relationships between variables, such as marketing budget and sales. There are other approaches to consider as well.

Leveraging technology. You may be able to use software you already own to generate sales forecasts. For example, many customer relationship management platforms offer reporting functions that can help with forecasting. There’s also dedicated sales forecasting software available. Artificial intelligence is having a major positive impact on these products.

Continuous improvement

If your company is already generating sales forecasts, give yourself some credit. However, remember that you must continuously improve your current process to refine its accuracy, adapt to changes and incorporate evolving best practices. FMD can help you create a sales forecasting process or improve the one you have in place.

How to Evaluate and Undertake a Business Transformation

Many industries have undergone monumental changes over the last decade or so. Broadly, there are two ways to adapt to the associated challenges: slowly or quickly.

Although there’s much to be said about small, measured responses to economic change, some companies might want to undertake a more urgent, large-scale revision of their operations. This is called a “business transformation” and, under the right circumstances, it can be a prudent move.

Defining the concept

A business transformation is a strategically planned modification of how all or part of a company operates. In its broadest form, a transformation might change the very mission of the business. For example, a financial consulting firm might become a software provider. However, there are other more subtle variations, including:

Digital transformation (implementing new technologies to digitalize every business function),

Operational transformation (streamlining workflows or revising processes to change operations fundamentally), and

Structural transformation (altering the leadership structure or reorganizing departments/units).

The overarching goal of any transformation is to boost the company’s financial performance by increasing efficiencies, improving customer service, seizing greater market share or entering a new market.

Making the call

Choosing to undertake a business transformation of any kind is a major decision. Before making the call, you and your leadership team must evaluate your company’s market position and identify what’s inhibiting growth and possibly even leading toward a downturn. Common indicators that a transformation may be needed include:

Declining revenues with little to no projections of upswings,

Outdated processes that are creating errors and upsetting customers,

Intensifying competition that will be difficult or impossible to counter, and

Shifts in customer expectations or demand that call for substantive changes.

To decide whether a business transformation is appropriate, you must conduct due diligence through measures such as analyzing financial data and market trends, gathering customer feedback, and obtaining the counsel of professional advisors.

5 general steps to follow

So, let’s say you do your due diligence and decide to move forward with a business transformation. Generally, companies follow five steps:

1. Set a clearly worded objective. The more specific you are in describing how you intend to transform your business, the more likely you are to accomplish that objective. Set aside the time and exercise the patience needed to find specificity and consensus with your leadership team, key employees and professional advisors.

2. Forecast the financial, legal and operational impacts. You must paint a realistic picture of how the big change will likely affect the business during and after the transformation. This is another step in which your professional advisors are critical. With their help, generate financial forecasts related to expenses and revenue changes, identify potential compliance risks and so forth.

3. Map out the road ahead. With a clear vision in mind and a wealth of information in hand, create a detailed roadmap to the transformation. A phased approach is typically best. Define milestones and align performance metrics to each phase. In addition, develop contingency plans in case you wander off course.

4. Communicate with stakeholders. Devise a communication strategy that addresses all key stakeholders — including employees, independent contractors, customers, vendors, suppliers, investors and lenders. Tailor the strategy to each audience, promoting transparency and encouraging buy-in.

5. Monitor progress and adapt as necessary. To increase your odds of success, you and your leadership team need to “stay on it.” Track metrics, allocate time to discussing progress, and be ready to overcome internal and external challenges.

Bold move

Business transformations are difficult to achieve. Insufficient planning, lack of financial oversight and employee resistance can derail efforts. Meanwhile, the necessary investments may strain cash flow. Worst of all, if you fail, you’ll have squandered all those resources.

On a more positive note, a successful business transformation can be a bold and powerful move toward achieving substantial growth and resilience. If you’re considering one, FMD can help you evaluate the concept and undertake the appropriate financial analyses.

Companies can Shine a Light on Financial Uncertainty with Flash Reports

Managing the financial performance of your business may sometimes seem like steering a ship through treacherous waters. Perhaps your voyage goes smoothly for a while until, quite suddenly, you hit a concerning dip or abrupt swell — either of which creates considerable operational pressure.

Your financial statements should provide keen insights into how your company is performing and where it’s headed. However, you probably generate them only monthly, quarterly or annually. That leaves lots of time in between when you may be sailing through a fog of uncertainty. Creating flash reports is one way to shine a light on the situation.

Take a snapshot

A flash report is a brief summary of a business’s current financial performance based on a few carefully selected metrics. The word “flash” is meant to evoke a camera taking a snapshot of key figures, such as cash balances, receivables aging, collections and payroll.

During seasonal peaks or when undertaking a turnaround, some companies create daily flash reports to track key activities such as sales, shipments and deposits. Otherwise, businesses generally create weekly or monthly reports, depending on their needs.

Flash reports should be as simple as possible. Those that take longer than an hour to prepare or take up more than one page are likely too complex. Flash reports should also be comparative — that is, they need to note significant trends or budgetary deviations that may call for corrective action.

Including graphs or tables can help nonfinancial staff who receive the reports, such as marketing and operations managers, read them more easily.

Use as directed

Flash reports can help you and your leadership team better catch and respond to financial performance developments that demand your attention. However, they have limitations.

First and foremost, flash reports provide a rough measure of financial performance within a short period. Therefore, they may not give a completely accurate picture of where your business stands. It’s common for items such as cash balances and collections to ebb and flow throughout the month, depending on billing cycles. So, you and your fellow report users must guard against overreaction.

Because of their “quick and dirty” nature, flash reports are best used for internal purposes only. Most companies don’t share them with investors, creditors or franchisors unless required under a bankruptcy or franchise agreement.

The risk is real: If shared flash reports deviate from what’s subsequently reported on your financial statements, stakeholders may wonder whether you’re:

Exaggerating financial performance,

Running into serious problems, or

Mismanaging your financial reporting.

That said, some lenders may ask for flash reports if a borrower fails to meet liquidity, profitability or leverage covenants. Should you decide to share reports for any reason, consider adding a disclaimer that the results are preliminary, may contain errors or omissions, and haven’t been prepared in accordance with U.S. Generally Accepted Accounting Principles (if you normally do so).

Get the info you need

Although you can probably find some flash report templates online, proceed cautiously. It’s imperative to design yours to provide the most relevant data for your company in the most readable format for your users. You may also need to occasionally revise the content and look of reports to keep up with changes to your business. Contact FMD for help developing flash reports, evaluating your current ones or improving any aspect of your financial reporting.

Choosing the Right Sales Compensation Model for Your Business

A strong sales team is the driving force of most small to midsize businesses. Strong revenue streams are hard to come by without skilled and engaged salespeople.

But what motivates these valued employees? First and foremost, equitable and enticing compensation. And therein lies a challenge for many companies: Choosing the right sales compensation model isn’t easy and may call for regular reevaluation. Let’s review some of the most popular models and note a recent trend.

Straight salary (or hourly wages)

The simplest way to pay sales staff is to offer a “straight salary,” meaning no commissions or other incentives are involved. (Some businesses may pay hourly wages instead, though this generally occurs only in a retail environment.)

The straight salary model’s advantage is that it’s easy for the company to administer and keeps payroll expenses predictable. It also provides financial stability for employees. The approach tends to work best in industries with long sales cycles and for particularly collaborative sales teams.

As you may have guessed, the downside is that it offers no financial incentive for salespeople to go beyond the status quo. This can result in flat sales and difficulty drawing new customers.

Commission only

Quite the opposite is the commission-only model. Here, sales team members earn income as a predetermined percentage of sales revenue. There are various ways to do this, but the bottom line is that staffers are compensated purely through sales wins; they don’t receive salaries.

The advantage is that they’re strongly motivated to succeed — one could even say it’s a “do or die” approach. This model often suits start-ups or businesses looking for quick growth without a big payroll budget. The risk for companies is that commission-only positions tend to have high turnover rates because salespeople lack income stability and may change jobs frequently.

Salary plus commission

Traditionally, this has been among the most popular compensation models. It combines the stability of a salary with the financial incentive of commissions. Generally, the salary will be relatively lower because sales staffers can make up the difference through the commissions.

For the business, this model may reduce turnover while still helping motivate employees. Its chief downsides are that salaries add to payroll expenses, and there’s a relatively high degree of administrative complexity involved in tracking and calculating commissions.

Salary plus performance-based incentives (hybrid)

If you’re interested in “what’s hot” in sales compensation, look no further. This model is often called “hybrid” because it combines a salary with various performance-based incentives tailored to the company’s needs.

Just last month, cloud-based sales software provider Xactly released the results of its annual Sales Compensation Report. Of 160 companies surveyed, 62% identified performance-based pay structures for sales reps as the biggest factor driving changes to sales compensation.

Like “base salary plus commission,” a hybrid model offers employees income stability — but it allows them to earn much more through multiple incentives. For businesses, the model may strengthen employee retention while motivating sales team members to meet targeted strategic objectives, such as increasing market share or driving top-line growth.

Companies have a wide variety of performance-based incentives to choose from, including:

Financial bonuses for acquiring new customers or expanding into new territories,

Profit-sharing plans that tie additional compensation to the company’s overall success, and

Long-term incentives, such as stock options, restricted stock units and performance shares.

However, it’s critical to design a hybrid model carefully. One major risk is becoming “a victim of your own success” — that is, running into cash flow problems because you must pay salespeople substantial amounts for earning the incentives offered.

No pressure

If your sales compensation model works well, don’t feel pressured to change it just to keep up with the Joneses. However, as your business grows, you may want to adjust or revise it to sustain or, better yet, increase that growth. FMD can help you evaluate your current model and make necessary adjustments that fit your company’s needs and budget.

Businesses have Options for Technology Leadership Positions

To say that technology continues to affect how businesses operate and interact with customers and prospects would be an understatement. According to the Business Software Market Size report issued by market researchers Mordor Intelligence, the global market size for commercial software is projected to reach $650 million this year and $1.10 trillion by 2029.

And that’s just software. Companies must also contend with technological issues such as hardware, skilled labor, strategy and cybersecurity. Just one of the resulting demands that this pressure is putting on businesses is a keen need for tech leadership.

If your company has grown to the point where it could use an executive-level employee with specialized knowledge of and laser focus on technology issues, you have plenty of options.

Positions to consider

Here are some of the most widely used position titles for technology executives:

Chief Information Officer (CIO). This person is typically responsible for managing a company’s internal IT infrastructure and operations. In fact, an easy way to remember the purpose of this position is to replace the word “Information” with “Internal.” A CIO’s job is to oversee the purchase, implementation and proper use of technological systems and products that will maximize the efficiency and productivity of the business.

Chief Technology Officer (CTO). In contrast to a CIO, a CTO focuses on external processes — specifically with customers and vendors. This person usually oversees the development and eventual production of technological products or services that will meet customer needs and increase revenue. The position demands the ability to live on the cutting edge by doing constant research into tech trends while also being highly collaborative with employees and vendors.

Chief Digital Officer (CDO). For some companies, the CIO and/or CTO are so busy with their respective job duties that they’re unable to look very far ahead. This is where a CDO typically comes into play. The primary purpose of this position is to spot new markets, channels or even business models that the company can target, explore and perhaps eventually profit from. So, while a CIO looks internally and a CTO looks externally, a CDO’s gaze is set on a more distant horizon.

Chief Artificial Intelligence Officer (CAIO). Did you really think you were going to make it through a technology article without reading about AI? Yes, more and more businesses are taking on executives whose primary responsibility is to create the company’s overall AI strategy and ensure it:

Aligns with the business’s overall strategic goals, and

Enhances the company’s digital transformation, which many businesses are continuing to undergo as they adapt to new technologies.

CAIOs are also typically responsible for understanding the global and national regulatory environments regarding AI, as well as ensuring the business uses AI ethically.

Big decision