BLOG

Building customers’ trust in your website

The events of the past year have taught business owners many important lessons. One of them is that, when a crisis hits, customers turn on their computers and look to their phones. According to one analysis of U.S. Department of Commerce data, consumers spent $347.26 billion online with U.S. retailers in the first half of 2020 — that’s a 30.1% increase from the same period in 2019.

Although online spending moderated a bit as the year went on, the fact remains that people’s expectations of most companies’ websites have soared. In fact, a June 2020 report by software giant Adobe indicated that the pandemic has markedly accelerated the growth of e-commerce — quite possibly by years, not just months.

Whether you sell directly to the buying public or engage primarily in B2B transactions, building customers’ trust in your website is more important than ever.

Identify yourself

Among the simplest ways to establish trust with customers and prospects is to convey to them that you’re a bona fide business staffed by actual human beings.

Include an “About Us” page with the names, photos and short bios of the owner(s), executives and key staff members. Doing so will help make the site friendlier and more relatable. You don’t want to look anonymous — it makes customers suspicious and less likely to buy.

Beyond that, be sure to clearly provide contact info. This includes a phone number and email address, hours of operation (including time zone), and your mailing address. If you’re a small business, use a street address if possible. Some companies won’t deliver to a P.O. box, and some customers won’t buy if you use one.

Keep contact links easy to find. No one wants to search all over a site looking for a way to get in touch with someone at the business. Include at least one contact link on every page.

Add trust elements

Another increasingly critical feature of business websites is “trust elements.” Examples include:

Icons of widely used payment security providers such as PayPal, Verisign and Visa,

A variety of payment alternatives, as well as free shipping or lower shipping costs for certain orders, and

Professionally coded, aesthetically pleasing and up-to-date layout and graphics.

Check and double-check the spelling and grammar used on your site. Remember, one of the hallmarks of many Internet scams is sloppy or nonsensical use of language.

Also, regularly check all links. Nothing sends a customer off to a competitor more quickly than the frustration of encountering nonfunctioning links. Such problems may also lead visitors to think they’ve been hacked.

Abide by the fundamentals

Of course, the cybersecurity of any business website begins (and some would say ends) with fundamental elements such as a responsible provider, firewalls, encryption software and proper password use. Nonetheless, how you design, maintain and update your site will likely have a substantial effect on your company’s profitability. Contact us for help measuring and assessing the impact of e-commerce on your business.

© 2021

What are the tax implications of buying or selling a business?

Merger and acquisition activity in many industries slowed during 2020 due to COVID-19. But analysts expect it to improve in 2021 as the country comes out of the pandemic. If you are considering buying or selling another business, it’s important to understand the tax implications.

Two ways to arrange a deal

Under current tax law, a transaction can basically be structured in two ways:

1. Stock (or ownership interest). A buyer can directly purchase a seller’s ownership interest if the target business is operated as a C or S corporation, a partnership, or a limited liability company (LLC) that’s treated as a partnership for tax purposes.

The current 21% corporate federal income tax rate makes buying the stock of a C corporation somewhat more attractive. Reasons: The corporation will pay less tax and generate more after-tax income. Plus, any built-in gains from appreciated corporate assets will be taxed at a lower rate when they’re eventually sold.

The current law’s reduced individual federal tax rates have also made ownership interests in S corporations, partnerships and LLCs more attractive. Reason: The passed-through income from these entities also is taxed at lower rates on a buyer’s personal tax return. However, current individual rate cuts are scheduled to expire at the end of 2025, and, depending on actions taken in Washington, they could be eliminated earlier.

Keep in mind that President Biden has proposed increasing the tax rate on corporations to 28%. He has also proposed increasing the top individual income tax rate from 37% to 39.6%. With Democrats in control of the White House and Congress, business and individual tax changes are likely in the next year or two.

2. Assets. A buyer can also purchase the assets of a business. This may happen if a buyer only wants specific assets or product lines. And it’s the only option if the target business is a sole proprietorship or a single-member LLC that’s treated as a sole proprietorship for tax purposes.

Preferences of buyers

For several reasons, buyers usually prefer to buy assets rather than ownership interests. In general, a buyer’s primary goal is to generate enough cash flow from an acquired business to pay any acquisition debt and provide an acceptable return on the investment. Therefore, buyers are concerned about limiting exposure to undisclosed and unknown liabilities and minimizing taxes after a transaction closes.

A buyer can step up (increase) the tax basis of purchased assets to reflect the purchase price. Stepped-up basis lowers taxable gains when certain assets, such as receivables and inventory, are sold or converted into cash. It also increases depreciation and amortization deductions for qualifying assets.

Preferences of sellers

In general, sellers prefer stock sales for tax and nontax reasons. One of their objectives is to minimize the tax bill from a sale. That can usually be achieved by selling their ownership interests in a business (corporate stock or partnership or LLC interests) as opposed to selling assets

With a sale of stock or other ownership interest, liabilities generally transfer to the buyer and any gain on sale is generally treated as lower-taxed long-term capital gain (assuming the ownership interest has been held for more than one year).

Obtain professional advice

Be aware that other issues, such as employee benefits, can also cause tax issues in M&A transactions. Buying or selling a business may be the largest transaction you’ll ever make, so it’s important to seek professional assistance. After a transaction is complete, it may be too late to get the best tax results. Contact us about how to proceed.

© 2021

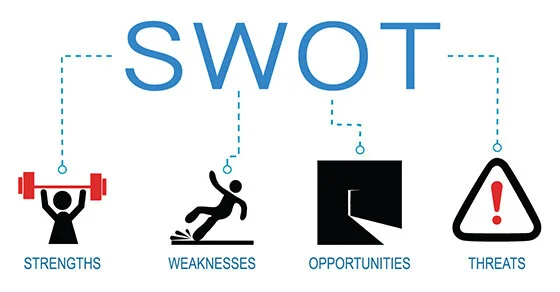

The many uses of a SWOT analysis

Using a strengths, weaknesses, opportunities and threats (SWOT) analysis to frame an important business decision is a long-standing recommended practice. But don’t overlook other, broader uses that could serve your company well.

Performance factors

A SWOT analysis starts by spotlighting internal strengths and weaknesses that affect business performance. Strengths are competitive advantages or core competencies that generate value (and revenue), such as a strong sales force or exceptional quality.

Conversely, weaknesses are factors that limit a company’s performance. These are often revealed in a comparison with competitors. Examples might include a negative brand image because of a recent controversy or an inferior reputation for customer service.

Generally, the strengths and weaknesses of a business relate directly to customers’ needs and expectations. Each identified characteristic affects cash flow — and, therefore, business success — if customers perceive it as either a strength or weakness. A characteristic doesn’t really affect the company if customers don’t care about it.

External conditions

The next SWOT step is identifying opportunities and threats. Opportunities are favorable external conditions that could generate a worthwhile return if the business acts on them. Threats are external factors that could inhibit business performance.

When differentiating strengths from opportunities, or weaknesses from threats, the question is whether the issue would exist without the business. If the answer is yes, the issue is external to the company and, therefore, an opportunity or a threat. Examples include changes in demographics or government regulations.

Various applications

As mentioned, business owners can use SWOT to do more than just make an important decision. Other applications include:

Valuation. A SWOT analysis is a logical way to frame a discussion of business operations in a written valuation report. The analysis can serve as a powerful appendix to the report or a courtroom exhibit, providing tangible support for seemingly ambiguous, subjective assessments regarding risk and return.

In a valuation context, strengths and opportunities generate returns, which translate into increased cash flow projections. Strengths and opportunities can lower risk via higher pricing multiples or reduced cost of capital. Threats and weaknesses have the opposite effect.

Strategic planning. Businesses can repurpose the SWOT analysis section of a valuation report to spearhead strategic planning. They can build value by identifying ways to capitalize on opportunities with strengths or brainstorming ways to convert weaknesses into strengths or threats into opportunities. You can also conduct a SWOT analysis outside of a valuation context to accomplish these objectives.

Legal defense. Should you find yourself embroiled in a legal dispute, an attorney may want to frame trial or deposition questions in terms of a SWOT analysis. Attorneys sometimes use this approach to demonstrate that an expert witness truly understands the business — or, conversely, that the opposing expert doesn’t understand the subject company.

Tried and true

A SWOT analysis remains a useful way to break down and organize the many complexities surrounding a business. Our firm can help you with the tax, accounting and financial aspects of this approach.

© 2021

Many tax amounts affecting businesses have increased for 2021

A number of tax-related limits that affect businesses are annually indexed for inflation, and many have increased for 2021. Some stayed the same due to low inflation. And the deduction for business meals has doubled for this year after a new law was enacted at the end of 2020. Here’s a rundown of those that may be important to you and your business.

Social Security tax

The amount of employees’ earnings that are subject to Social Security tax is capped for 2021 at $142,800 (up from $137,700 for 2020).

Deductions

Section 179 expensing:

Limit: $1.05 million (up from $1.04 million for 2020)

Phaseout: $2.62 million (up from $2.59 million)

Income-based phase-out for certain limits on the Sec. 199A qualified business income deduction begins at:

Married filing jointly: $329,800 (up from $326,600)

Married filing separately: $164,925 (up from $163,300)

Other filers: $164,900 (up from $163,300)

Business meals

Deduction for eligible business-related food and beverage expenses provided by a restaurant: 100% (up from 50%)

Retirement plans

Employee contributions to 401(k) plans: $19,500 (unchanged from 2020)

Catch-up contributions to 401(k) plans: $6,500 (unchanged)

Employee contributions to SIMPLEs: $13,500 (unchanged)

Catch-up contributions to SIMPLEs: $3,000 (unchanged)

Combined employer/employee contributions to defined contribution plans: $58,000 (up from $57,000)

Maximum compensation used to determine contributions: $290,000 (up from $285,000)

Annual benefit for defined benefit plans: $230,000 (up from $225,000)

Compensation defining a highly compensated employee: $130,000 (unchanged)

Compensation defining a “key” employee: $185,000 (unchanged)

Other employee benefits

Qualified transportation fringe-benefits employee income exclusion: $270 per month (unchanged)

Health Savings Account contributions:

Individual coverage: $3,600 (up from $3,550)

Family coverage: $7,200 (up from $7,100)

Catch-up contribution: $1,000 (unchanged)

Flexible Spending Account contributions:

Health care: $2,750 (unchanged)

Dependent care: $5,000 (unchanged)

These are only some of the tax limits that may affect your business and additional rules may apply. If you have questions, please contact us.

© 2021

Are your supervisors adept at multigenerational management?

Over the past year, the importance of leadership at every level of a business has been emphasized. When a crisis such as a pandemic hits, it creates a sort of stress test for not only business owners and executives, but also supervisors of departments and work groups.

Among the most important skill sets of any leader is communication. Can your company’s supervisors communicate both the big and little picture messages that will keep employees reassured, focused and motivated during good times and bad? One factor in their ability to do so is the age of the employees with whom they’re interacting.

Encourage a flexible management style

Right now, there may be four different generations in your workplace: 1) Baby Boomers, born following World War II through the mid-1960s, 2) Generation X, born from the mid-1960s through the late 1970s, 3) Millennials, born from the late 1970s through the mid-1990s, and 4) Generation Z, born in the mid-1990s and beyond. (Birth dates for each generation may vary depending on the source.)

Supervisors need to develop a flexible style when dealing with multiple generations. Millennial and Generation Z employees tend to have different needs and expectations than Baby Boomers and those in Generation X.

For example, Millennials and Gen Z employees generally like to receive more regular feedback about their performances, as well as more frequent public recognition when they’ve done well. Baby Boomers and Gen Xers also enjoy positive performance feedback, but they may expect praise less often and derive personal satisfaction from a job well done without needing to share it with co-workers quite as often.

Employees from different generations also tend to have differing views on company loyalty. Many younger employees harbor greater allegiance to their principles and co-workers than their employers, while many older employees feel a greater sense of fidelity to the business itself. Train your supervisors to keep these and other differences in mind when managing employees across generations.

Recognize the impact of benefits

While financial security is highly valued by every generation, younger employees (Millennials and Gen Z) may prioritize salary less than older workers. What’s often more important to recent generations is a robust, well-rounded benefits package.

Of particular importance is mental health care. Whereas older generations may have historically approached mental health issues with hesitancy, and some still do, younger generations generally prioritize psychological well-being quite openly. Business owners should keep this in mind when designing and adjusting their benefits plans, and supervisors (and HR departments) need to encourage and guide employees to optimally use their benefits.

Promote workplace harmony

To be clear, a person’s generation doesn’t necessarily define him or her, nor is it a perfect predictor of how someone thinks or behaves. Nevertheless, supervisors who are aware of generational differences can develop more flexible, dynamic management styles. Doing so can lead to a more harmonious, productive workplace — and a more profitable business. We can assist you in developing cost-effective strategies for upskilling supervisors and maximizing productivity.

© 2021

View your financial statements through the right lens

Many business owners generate financial statements, at least in part, because lenders and other stakeholders demand it. You’re likely also aware of how insightful properly prepared financial statements can be — especially when they follow Generally Accepted Accounting Principles.

But how can you best extract these useful insights? One way is to view your financial statements through a wide variety of “lenses” provided by key performance indicators (KPIs). These are calculations or formulas into which you can plug numbers from your financial statements and get results that enable you to make better business decisions.

Learn about liquidity

If you’ve been in business for any amount of time, you know how important it is to be “liquid.” Companies must have sufficient current assets to meet their current obligations. Cash is obviously the most liquid asset, followed by marketable securities, receivables and inventory.

Working capital — the difference between current assets and current liabilities — is a quick and relatively simple KPI for measuring liquidity. Other KPIs that assess liquidity include working capital as a percentage of total assets and the current ratio (current assets divided by current liabilities). A more rigorous benchmark is the acid (or quick) test, which excludes inventory and prepaid assets from the equation.

Accentuate asset awareness

Businesses are more than just cash; your assets matter too. Turnover ratios, a form of KPI, show how efficiently companies manage their assets. Total asset turnover (sales divided by total assets) estimates how many dollars in revenue a company generates for every dollar invested in assets. In general, the more dollars earned, the more efficiently assets are used.

Turnover ratios also can be measured for each specific category of assets. For example, you can calculate receivables turnover ratios in terms of days. The collection period equals average receivables divided by annual sales multiplied by 365 days. A collection period of 45 days indicates that the company takes an average of one and one-half months to collect invoices.

Promote profitability

Liquidity and asset management are critical, but the bottom line is the bottom line. When it comes to measuring profitability, public companies tend to focus on earnings per share. But private businesses typically look at profit margin (net income divided by revenue) and gross margin (gross profits divided by revenue).

For meaningful comparisons, you’ll need to adjust for nonrecurring items, discretionary spending and related-party transactions. When comparing your business to other companies with different tax strategies, capital structures or depreciation methods, it may be useful to compare earnings before interest, taxes, depreciation and amortization (EBITDA).

Focus in

As your business grows, your financial statements may contain so much information that it’s hard to know what to focus on. Well-chosen and accurately calculated KPIs can reveal important trends and developments. Contact us with any questions you might have about generating sound financial statements and getting the most out of them.

© 2021

The cents-per-mile rate for business miles decreases again for 2021

This year, the optional standard mileage rate used to calculate the deductible costs of operating an automobile for business decreased by one-and-one-half cents, to 56 cents per mile. As a result, you might claim a lower deduction for vehicle-related expenses for 2021 than you could for 2020 or 2019. This is the second year in a row that the cents-per-mile rate has decreased.

Deducting actual expenses vs. cents-per-mile

In general, businesses can deduct the actual expenses attributable to business use of vehicles. This includes gas, oil, tires, insurance, repairs, licenses and vehicle registration fees. In addition, you can claim a depreciation allowance for the vehicle. However, in many cases, certain limits apply to depreciation write-offs on vehicles that don’t apply to other types of business assets.

The cents-per-mile rate is useful if you don’t want to keep track of actual vehicle-related expenses. With this method, you don’t have to account for all your actual expenses. However, you still must record certain information, such as the mileage for each business trip, the date and the destination.

Using the cents-per-mile rate is also popular with businesses that reimburse employees for business use of their personal vehicles. These reimbursements can help attract and retain employees who drive their personal vehicles extensively for business purposes. Why? Under current law, employees can no longer deduct unreimbursed employee business expenses, such as business mileage, on their own income tax returns.

If you do use the cents-per-mile rate, be aware that you must comply with various rules. If you don’t comply, the reimbursements could be considered taxable wages to the employees.

The 2021 rate

Beginning on January 1, 2021, the standard mileage rate for the business use of a car (van, pickup or panel truck) is 56 cents per mile. It was 57.5 cents for 2020 and 58 cents for 2019.

The business cents-per-mile rate is adjusted annually. It’s based on an annual study commissioned by the IRS about the fixed and variable costs of operating a vehicle, such as gas, maintenance, repair and depreciation. The rate partly reflects the current price of gas, which is down from a year ago. According to AAA Gas Prices, the average nationwide price of a gallon of unleaded regular gas was $2.42 recently, compared with $2.49 a year ago. Occasionally, if there’s a substantial change in average gas prices, the IRS will change the cents-per-mile rate midyear.

When this method can’t be used

There are some situations when you can’t use the cents-per-mile rate. In some cases, it partly depends on how you’ve claimed deductions for the same vehicle in the past. In other cases, it depends on if the vehicle is new to your business this year or whether you want to take advantage of certain first-year depreciation tax breaks on it.

As you can see, there are many factors to consider in deciding whether to use the mileage rate to deduct vehicle expenses. We can help if you have questions about tracking and claiming such expenses in 2021 — or claiming them on your 2020 income tax return.

© 2021

The new Form 1099-NEC and the revised 1099-MISC are due to recipients soon

There’s a new IRS form for business taxpayers that pay or receive certain types of nonemployee compensation and it must be furnished to most recipients by February 1, 2021. After sending the forms to recipients, taxpayers must file the forms with the IRS by March 1 (March 31 if filing electronically).

The requirement begins with forms for tax year 2020. Payers must complete Form 1099-NEC, “Nonemployee Compensation,” to report any payment of $600 or more to a recipient. February 1 is also the deadline for furnishing Form 1099-MISC, “Miscellaneous Income,” to report certain other payments to recipients.

If your business is using Form 1099-MISC to report amounts in box 8, “substitute payments in lieu of dividends or interest,” or box 10, “gross proceeds paid to an attorney,” there’s an exception to the regular due date. Those forms are due to recipients by February 16, 2021.

1099-MISC changes

Before the 2020 tax year, Form 1099-MISC was filed to report payments totaling at least $600 in a calendar year for services performed in a trade or business by someone who isn’t treated as an employee (in other words, an independent contractor). These payments are referred to as nonemployee compensation (NEC) and the payment amount was reported in box 7.

Form 1099-NEC was introduced to alleviate the confusion caused by separate deadlines for Form 1099-MISC that reported NEC in box 7 and all other Form 1099-MISC for paper filers and electronic filers.

Payers of nonemployee compensation now use Form 1099-NEC to report those payments.

Generally, payers must file Form 1099-NEC by January 31. But for 2020 tax returns, the due date is February 1, 2021, because January 31, 2021, is on a Sunday. There’s no automatic 30-day extension to file Form 1099-NEC. However, an extension to file may be available under certain hardship conditions.

When to file 1099-NEC

If the following four conditions are met, you must generally report payments as nonemployee compensation:

You made a payment to someone who isn’t your employee,

You made a payment for services in the course of your trade or business,

You made a payment to an individual, partnership, estate, or, in some cases, a corporation, and

You made payments to a recipient of at least $600 during the year.

We can help

If you have questions about filing Form 1099-NEC, Form 1099-MISC or any tax forms, contact us. We can assist you in staying in compliance with all rules.

© 2021

Getting more for your marketing dollars in 2021

A new year has arrived and, with it, a fresh 12 months of opportunities to communicate with customers and prospects. Like every year, 2021 brings distinctive marketing trends to the table. The COVID-19 pandemic and resulting economic challenges continue to drive the conversation in most industries. To get more for your marketing dollars, you’ll need to tailor your message to this environment.

Continue to invest in digital

There’s good reason to remind yourself of digital marketing’s continuing value in our brave new world of daily videoconferencing and booming online shopping. It’s affordable and allows you to communicate with customers directly. In addition, it provides faster results and better tracking capabilities.

Consider or re-evaluate strategies such as regularly updating your search engine optimization so your website ranks highly in online searches and more people can find you. Adjust your use of email, text messages and social media to communicate with customers and prospects.

For instance, craft more dynamic messages to introduce new products or special events. Offer “flash sales” and Internet-only deals to test and tweak offers before making them via more expansive (and expensive) media.

Seek out better deals

During boom times, you may feel at the mercy of high advertising rates. In the current uncertain and gradually recovering economy, look for better deals. The good news is that there are many more marketing/advertising channels than there used to be and, therefore, much more competition among them. Paying less is often a matter of knowing where to look.

Track your marketing efforts carefully and dedicate time to exploring new options. For example, podcasts remain enormously popular. Could a marketing initiative that exploits their reach pay dividends? Another possibility is shifting to smaller, less expensive ads posted in a wider variety of outlets rather than engaging in one massive campaign.

Excel at public relations

When the pandemic hit last year, every business had to address current events in their marketing messaging. This stood in stark contrast to decades previous, when companies generally tended to steer clear of the news. Nowadays, public relations is a key component of marketing success. Your customers and prospects need to know that your business is aware of the current environment and adjusting to it.

Ask your marketing department to craft clear, concise but exciting press releases regarding your newest products or services. Then distribute these press releases via both traditional and online channels to complement your marketing efforts. In this manner, you can disseminate trustworthy information and maintain a strong reputation — all at a relatively low cost.

Strengthen ROI

Your company’s marketing dollars need to provide a return on investment just as robust as its budget for production, employment and other key areas. Our firm can help you evaluate your marketing efforts from a financial perspective and identify ways to make those dollars go further.

© 2021

Blockchain beckons businesses … still

The term and concept known as “blockchain” is hardly new. This technology surfaced more than a decade ago. Bitcoin, the relatively well-known form of cryptocurrency, has gotten much more attention than blockchain itself, which is the platform on which Bitcoin is exchanged.

One might be tempted to think that, having spent so many years in the shadows, blockchain has missed its opportunity to become widely accepted by businesses. Yet its promise persists, and you’d be well-advised to keep an eye on when blockchain might begin to make further inroads into your industry — if it hasn’t already.

A shared ledger

In simple terms, blockchain is a distributed, shared ledger that’s continuously copied and synchronized to thousands of computers. These so-called “nodes” are part of a public or private network.

The ledger isn’t housed on a central server or controlled by any one party. Rather, transactions are added to the ledger only when they’re verified through established consensus protocols. Third-party verification makes blockchain highly resistant to errors, tampering or fraud. The technology uses encryption and digital signatures to ensure participants’ identities aren’t disclosed without permission.

Smart contracts

Blockchain’s ability to produce indelible, validated records establishes trust without the need for intermediaries to settle or authenticate transactions. So, the technology lends itself to a wide variety of uses.

Perhaps the most talked-about functionality of blockchain is smart contracts. These allow parties to create and execute contracts directly using blockchain, with less involvement by lawyers or other intermediaries.

For example, under a simple lease agreement, a business might lease office space through blockchain, paying the deposit and rent in Bitcoin or another cryptocurrency. The system automatically generates a receipt, which is held in a virtual contract between the parties. It’s impossible for either party to tamper with the lease document without the other party being alerted.

The landlord provides the lessee with a digital entry key, and the funds are released to the landlord. If the landlord fails to provide the key by the specified date, the system automatically processes a refund.

Legal protection

Business owners may also encounter blockchain when looking to exercise, secure or defend their legal rights. In litigation, demonstrating that “service of process” has been completed or attempted can be a challenge. Some companies are using blockchain to address this issue.

Process servers in the field use an app to post metadata — such as GPS coordinates, timestamps and device data — to a blockchain, which generates a unique identification code. Lawyers, courts and other interested parties can use the blockchain ID to access service of process data and confirm that information in physical affidavits or other records hasn’t been altered.

Stay tuned

Blockchain continues to beckon forward-thinking business owners with its ability to provide highly efficient and secure transactions — particularly for companies that do business internationally. We can assist you in identifying whether this or other technologies may enable you to better manage your company’s finances.

© 2021

Ring in the new year with a renewed focus on profitability

Some might say the end of one calendar year and the beginning of another is a formality. The linear nature of time doesn’t change, merely the numbers we use to mark it.

Others, however, would say that a fresh 12 months — particularly after the arduous, anxiety-inducing nature of 2020 — creates the perfect opportunity for business owners to gather their strength and push ahead with greater vigor. One way to do so is to ring in the new year with a systematic approach to renewing everyone’s focus on profitability.

Create an idea-generating system

Without a system to discover ideas that originate from the day-in, day-out activities of your business, you’ll likely miss opportunities to truly maximize the bottom line. What you want to do is act in ways that inspire and allow you to gather profit-generating concepts. Then you can pick out the most actionable ones and turn them into bottom-line-boosting results. Here are some ways to create such a system:

Share responsibility for profitability with your management team. All too often, managers become trapped in their own information silos and areas of focus. Consider asking everyone in a leadership position to submit ideas for growing the bottom line.

Instruct supervisors to challenge their employees to come up with profit-building ideas. Leaving your employees out of the conversation is a mistake. Ask workers on the front lines how they think your business could make more money.

Target the proposed ideas that will most likely increase sales, cut costs or expand profit margins. As suggestions come in, use robust discussions and careful calculations to determine which ones are truly worth pursuing.

Tie each chosen idea to measurable financial goals. When you’ve picked one or more concepts to pursue in real life, identify which metrics will accurately inform you that you’re on the right track. Track these metrics regularly from start to finish.

Name those accountable for executing each idea. Every business needs its champions! Be sure each profit-building initiative has a defined leader and team members.

Follow a clear, patient and well-monitored implementation process. Ideas that ultimately do build the bottom line in a meaningful way generally take time to identify, implement and execute. Don’t look for quick-fix measures; seek out business transformations that will lead to long-term success.

Many benefits

A carefully constructed and strong-performing profitability idea system can not only grow the bottom line, but also upskill employees and improve morale as strategies come to fruition. Our firm can help you identify profit-building opportunities, choose the right metrics to evaluate and measure them, and track the pertinent data over time.

© 2020

2021 Q1 tax calendar: Key deadlines for businesses and other employers

Here are some of the key tax-related deadlines affecting businesses and other employers during the first quarter of 2021. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

January 15

Pay the final installment of 2020 estimated tax.

Farmers and fishermen: Pay estimated tax for 2020.

February 1 (The usual deadline of January 31 is a Sunday)

File 2020 Forms W-2, “Wage and Tax Statement,” with the Social Security Administration and provide copies to your employees.

Provide copies of 2020 Forms 1099-MISC, “Miscellaneous Income,” to recipients of income from your business where required.

File 2020 Forms 1099-MISC reporting nonemployee compensation payments in Box 7 with the IRS.

File Form 940, “Employer’s Annual Federal Unemployment (FUTA) Tax Return,” for 2020. If your undeposited tax is $500 or less, you can either pay it with your return or deposit it. If it’s more than $500, you must deposit it. However, if you deposited the tax for the year in full and on time, you have until February 10 to file the return.

File Form 941, “Employer’s Quarterly Federal Tax Return,” to report Medicare, Social Security and income taxes withheld in the fourth quarter of 2020. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the quarter in full and on time, you have until February 10 to file the return. (Employers that have an estimated annual employment tax liability of $1,000 or less may be eligible to file Form 944, “Employer’s Annual Federal Tax Return.”)

File Form 945, “Annual Return of Withheld Federal Income Tax,” for 2020 to report income tax withheld on all nonpayroll items, including backup withholding and withholding on accounts such as pensions, annuities and IRAs. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the year in full and on time, you have until February 10 to file the return.

March 1 (The usual deadline of February 28 is a Sunday)

File 2020 Forms 1099-MISC with the IRS if: 1) they’re not required to be filed earlier and 2) you’re filing paper copies. (Otherwise, the filing deadline is March 31.)

March 16

If a calendar-year partnership or S corporation, file or extend your 2020 tax return and pay any tax due. If the return isn’t extended, this is also the last day to make 2020 contributions to pension and profit-sharing plans.

© 2020

The right entity choice: Should you convert from a C to an S corporation?

The best choice of entity can affect your business in several ways, including the amount of your tax bill. In some cases, businesses decide to switch from one entity type to another. Although S corporations can provide substantial tax benefits over C corporations in some circumstances, there are potentially costly tax issues that you should assess before making the decision to convert from a C corporation to an S corporation.

Here are four issues to consider:

1. LIFO inventories. C corporations that use last-in, first-out (LIFO) inventories must pay tax on the benefits they derived by using LIFO if they convert to S corporations. The tax can be spread over four years. This cost must be weighed against the potential tax gains from converting to S status.

2. Built-in gains tax. Although S corporations generally aren’t subject to tax, those that were formerly C corporations are taxed on built-in gains (such as appreciated property) that the C corporation has when the S election becomes effective, if those gains are recognized within five years after the conversion. This is generally unfavorable, although there are situations where the S election still can produce a better tax result despite the built-in gains tax.

3. Passive income. S corporations that were formerly C corporations are subject to a special tax. It kicks in if their passive investment income (including dividends, interest, rents, royalties, and stock sale gains) exceeds 25% of their gross receipts, and the S corporation has accumulated earnings and profits carried over from its C corporation years. If that tax is owed for three consecutive years, the corporation’s election to be an S corporation terminates. You can avoid the tax by distributing the accumulated earnings and profits, which would be taxable to shareholders. Or you might want to avoid the tax by limiting the amount of passive income.

4. Unused losses. If your C corporation has unused net operating losses, they can’t be used to offset its income as an S corporation and can’t be passed through to shareholders. If the losses can’t be carried back to an earlier C corporation year, it will be necessary to weigh the cost of giving up the losses against the tax savings expected to be generated by the switch to S status.

Other considerations

When a business switches from C to S status, these are only some of the factors to consider. For example, shareholder-employees of S corporations can’t get all of the tax-free fringe benefits that are available with a C corporation. And there may be issues for shareholders who have outstanding loans from their qualified plans. These factors have to be taken into account in order to understand the implications of converting from C to S status.

If you’re interested in an entity conversion, contact us. We can explain what your options are, how they’ll affect your tax bill and some possible strategies you can use to minimize taxes.

© 2020

Prevent and detect insider cyberattacks

In one recent cybercrime scheme, a mortgage company employee accessed his employer’s records without authorization, then used stolen customer lists to start his own mortgage business. The perpetrator hacked the protected records by sending an email containing malware to a coworker.

This particular dishonest worker was caught. But your company may not be so lucky. One of your employees’ cybercrime schemes could end in financial losses or competitive disadvantages due to corporate espionage.

Best practices

Why would trusted employees steal from the hand that feeds them? They could be working for a competitor or seeking revenge for perceived wrongs. Sometimes coercion by a third party or the need to pay gambling or addiction-related debts comes into play.

Although there are no guarantees that you’ll be able to foil every hacking scheme, your business can minimize the risk of insider theft by implementing several best practices:

Restrict IT use. Your IT personnel should take proactive measures to restrict or monitor employee use of email accounts, websites, peer-to-peer networking, Instant Messaging protocols and File Transfer Protocol.

Remove access. When employees leave the company, immediately remove them from all access lists and ask them to return their means of access to secure accounts. Provide them with copies of any signed confidentiality agreements as a reminder of their legal responsibilities for maintaining data confidentiality.

Don’t neglect physical assets. Some data thefts occur the old-fashioned way — with employees absconding with materials after hours or while no one is looking. Typically, a crooked employee will print or photocopy documents and remove them from the workplace hidden in a briefcase or bag. Some dishonest employees remove files from cabinets, desks or other storage locations. Controls such as locks, surveillance cameras and restrictions to access can help prevent and deter theft.

Treat workers well. Create a positive work environment and treat employees fairly and with respect. This can encourage loyalty and trust, thereby minimizing potential motives for employee theft.

Wireless risk

In addition to the previously named threats, your office’s wireless communication networks — including Wi-Fi, Bluetooth and cellular — can increase fraud risk. Fraud perpetrators can, for example, use mobile devices to gain access to sensitive information. One way to deter such activities is to restrict Wi-Fi to employees with special passwords or biometric access.

For more tips on preventing employee-originated cybercrime, or if you suspect a fraud scheme is underway, contact us for help.

© 2020

Gig workers, know your tax responsibilities

Let’s say you drive for a ride-sharing app, deliver groceries ordered online or perform freelance home repairs booked via a mobile device. If you do one of these jobs or myriad others that are similar, you’re likely a gig worker — part of a growing segment of the economy. For taxpayers who’ve turned to gig work this year, due to losing their job during the COVID-19 crisis or some other reason, it’s critical that they understand the income tax consequences.

A different way

No matter what the job or app, all gig workers have one thing in common: income tax obligations. But the way you’ll pay taxes differs from the way you would as an employee.

To start, you’re typically considered self-employed. As a result, and because an employer isn’t withholding money from your paycheck to cover your tax obligations, you’re responsible for making federal income tax payments. Depending on where you live, you also may have to pay state income tax.

Quarterly tax payments

The U.S. income tax system is considered “pay as you go.” Self-employed individuals typically pay federal income tax four times during the year: generally, on April 15, June 15, and September 15 of the current year, and January 15 of the following year. (For 2020, the April 15 and June 15 deadlines were postponed to July 15 due to the pandemic. It’s possible other deadlines could be postponed, too.)

If you don’t pay enough over these four estimated tax installments to cover the required amount for the year, you may be subject to penalties. To minimize the risk of penalties, you must generally pay either 90% of the tax you’ll owe for the current year or 100% of the amount you paid the previous year (110% of your previous year’s tax if your adjusted gross income was more than $150,000 or, if married filing separately, more than $75,000).

The 1099

You may have encountered the term “the 1099 economy” or been called a “1099 worker.” This is because, as a self-employed person, you won’t get a W-2 from an employer. You may, however, receive a Form 1099 from any client or customer that paid you at least $600 throughout the year. The client sends the same form to the IRS, so it pays to monitor the 1099s you receive and verify that the amounts match your records.

If a client (say, a ride-sharing app) uses a third-party payment system, you might receive a Form 1099-K. Even if you didn’t earn enough from a client to receive a 1099, or you’re not sent a 1099-K, you’re still responsible for reporting the income you were paid. Keep in mind that typically you’re taxed on income when received, not when you send a request for payment.

Expense deductions

By definition, gig workers are self-employed. So, your income taxes are based on the profits left after you deduct business-related expenses from your revenue.

Expenses can include payment processing fees, your investment in office equipment and specific costs required to provide your service. If you use a portion of your home exclusively for workspace, you might be able to claim a home office deduction.

Good record keeping

As a gig worker, you need to keep accurate, timely records of your revenue and expenses so you pay the income taxes you owe — but no more. You also likely will have self-employment tax obligations (such as Medicare and Social Security taxes). Our firm can help you set up a good record keeping system, file your taxes and stay updated on new developments in the gig economy.

© 2020

5 tips for safe intrafamily loans

If a relative needs financial help, offering an intrafamily loan might seem like a good idea. But if not properly executed, such loans can carry negative tax consequences — such as unexpected taxable income, gift tax or both. Here are five tips to help avoid any unwelcome tax surprises:

1. Create a paper trail. In general, to avoid undesirable tax consequences, you need to be able to show that the loan was bona fide. To do so, document evidence of:

· The amount and terms of the debt,

· Interest charged,

· Fixed repayment schedules,

· Collateral,

· Demands for repayment, and

· The borrower’s solvency at the time of the loan.

Be sure to make your intentions clear — and help avoid loan-related misunderstandings — by also documenting the loan payments received.

2. Demonstrate an intention to collect. Even if you think you may eventually forgive the loan, ensure the borrower makes at least a few payments. By having some repayment history, you’ll make it harder for the IRS to argue that the loan was really an outright gift. And if a would-be borrower has no realistic chance of repaying a loan, don’t make it. If you’re audited, the IRS is sure to treat such a loan as a gift.

3. Charge interest if the loan exceeds $10,000. If you lend more than $10,000 to a relative, charge at least the applicable federal interest rate (AFR). Be aware that interest on the loan will be taxable income to you. If no or below-AFR interest is charged, taxable interest is calculated under the complicated below-market-rate loan rules. In addition, all of the forgone interest over the term of the loan may have to be treated as a gift in the year the loan is made. This will increase your chances of having to use some of your lifetime exemption.

4. Use the annual gift tax exclusion. If you want to, say, help your daughter buy a house but don’t want to use up any of your lifetime gift and estate tax exemption, you can make the loan and charge interest and then forgive the interest, the principal payments or both each year under the annual gift tax exclusion. For 2020, you can forgive up to $15,000 per borrower ($30,000 if your spouse joins in the gift) without paying gift taxes or using any of your lifetime exemption. But you will still have interest income in the year of forgiveness.

5. Forgive or file suit. If an intrafamily loan that you intended to collect is in default, don’t let it sit too long. To prove this was a legitimate loan that soured, you’ll need to take appropriate legal steps toward collection. If you know you’ll never collect and don’t want to file suit, begin forgiving the loan using the annual gift tax exclusion, if possible.

© 2020

Rightsizing your sales force

With a difficult year almost over, and another one on the horizon, now may be a good time to assess the size of your sales force. Maybe the economic changes triggered by the COVID-19 pandemic led you to downsize earlier in the year. Or perhaps you’ve added to your sales team to seize opportunities. In either case, every business owner should know whether his or her sales team is the right size.

Various KPIs

To determine your optimal sales staffing level, there are several steps you can take. A good place to start is with various key performance indicators (KPIs) that enable you to quantify performance in dollars and cents.

The KPIs you choose to calculate and evaluate need to be specific to your industry and appropriate to the size of your company and the state of the market in which you operate. If you’re comparing your sales numbers to those of other businesses, make sure it’s an apples-to-apples comparison.

In addition, you’ll need to pick KPIs that are appropriate to whether you’re assessing the performance of a sales manager or that of a sales representative. For a sales manager, you could look at average annual sales volume to determine whether his or her team is contributing adequately to your target revenue goals. Ideal KPIs for sales reps are generally more granular; examples include sales by rep and lead-to-sale percentage.

More than math

Rightsizing your sales staff, however, isn’t only a mathematical equation. To customize your approach, think about the specific needs of your company.

Consider, for example, how you handle staffing when sales employees take vacations or call in sick. If you frequently find yourself coming up short on revenue projections because of a lack of boots on the ground, you may want to expand your sales staff to cover territories and serve customers more consistently.

Then again, financial problems that arise from carrying too many sales employees can creep up on you. Be careful not to hire at a rate faster than your sales and gross profits are increasing. If you’re looking to make aggressive moves in your market, be sure you’ve done the due diligence to ensure that the hiring and training costs will likely pay off.

Last, but not least, think about your customers. Are they largely satisfied? If so, the size of your sales force might be just fine. However, salespeople saying that they’re overworked or customers complaining about a lack of responsiveness could mean your staff is too small. Conversely, if you have market segments that just aren’t yielding revenue or salespeople who are continually underperforming, it might be time to downsize.

Reasonable objectives

By regularly monitoring the headcount of your sales staff with an eye on fulfilling reasonable revenue goals, you’ll stand a better chance of maximizing profitability during good times and maintaining it during more challenging periods. Contact us for help choosing the right KPIs and cost-effectively managing your business.

© 2020

Drive more savings to your business with the heavy SUV tax break

Are you considering replacing a car that you’re using in your business? There are several tax implications to keep in mind.

A cap on deductions

Cars are subject to more restrictive tax depreciation rules than those that apply to other depreciable assets. Under so-called “luxury auto” rules, depreciation deductions are artificially “capped.” So is the alternative Section 179 deduction that you can claim if you elect to expense (write-off in the year placed in service) all or part of the cost of a business car under the tax provision that for some assets allows expensing instead of depreciation. For example, for most cars that are subject to the caps and that are first placed in service in calendar year 2020 (including smaller trucks or vans built on a truck chassis that are treated as cars), the maximum depreciation and/or expensing deductions are:

$18,100 for the first tax year in its recovery period (2020 for calendar year taxpayers);

$16,100 for the second tax year;

$9,700 for the third tax year; and

$5,760 for each succeeding tax year.

The effect is generally to extend the number of years it takes to fully depreciate the vehicle.

The heavy SUV strategy

Because of the restrictions for cars, you might be better off from a tax standpoint if you replace your business car with a heavy sport utility vehicle (SUV), pickup or van. That’s because the caps on annual depreciation and expensing deductions for passenger automobiles don’t apply to trucks or vans (and that includes SUVs). What type of SUVs qualify? Those that are rated at more than 6,000 pounds gross (loaded) vehicle weight.

This means that in most cases you’ll be able to write off the entire cost of a new heavy SUV used entirely for business purposes as 100% bonus depreciation in the year you place it into service. And even if you elect out of bonus depreciation for the heavy SUV (which generally would apply to the entire depreciation class the SUV belongs in), you can elect to expense under Section 179 (subject to an aggregate dollar limit for all expensed assets), the cost of an SUV up to an inflation-adjusted limit ($25,900 for an SUV placed in service in tax years beginning in 2020). You’d then depreciate the remainder of the cost under the usual rules without regard to the annual caps.

Potential caveats

The tax benefits described above are all subject to adjustment for non-business use. Also, if business use of an SUV doesn’t exceed 50% of total use, the SUV won’t be eligible for the expensing election, and would have to be depreciated on a straight-line method over a six-tax-year period.

Contact us if you’d like more information about tax breaks when you buy a heavy SUV for business.

© 2020

Should you add a technology executive to your staff?

The COVID-19 pandemic and resulting economic impact have hurt many companies, especially small businesses. However, for others, the jarring challenges this year have created opportunities and accelerated changes that were probably going to occur all along.

One particular area of speedy transformation is technology. It’s never been more important for businesses to wield their internal IT effectively, enable customers and vendors to easily interact with those systems, and make the most of artificial intelligence and “big data” to spot trends.

Accomplishing all this is a tall order for even the most energetic business owner or CEO. That’s why many companies end up creating one or more tech-specific executive positions. Assuming you don’t already employ such an individual, should you consider adding an IT exec? Perhaps so.

3 common positions

There are three widely used position titles for technology executives:

1. Chief Information Officer (CIO). This person is typically responsible for managing a company’s internal IT infrastructure and operations. In fact, an easy way to remember the purpose of this position is to replace the word “Information” with “Internal.” A CIO’s job is to oversee the purchase, implementation and proper use of technological systems and products that will maximize the efficiency and productivity of the business.

2. Chief Technology Officer (CTO). In contrast to a CIO, a CTO focuses on external processes — specifically, with customers and vendors. This person usually oversees the development and eventual production of technological products or services that will meet customer needs and increase revenue. The position demands the ability to live on the cutting edge by doing constant research into tech trends while also being highly collaborative with employees and vendors.

3. Chief Digital Officer (CDO). For some companies, the CIO and/or CTO are so busy with their respective job duties that they’re unable to look very far ahead. This is where a CDO typically comes into play. His or her primary objective is to spot new markets, channels or even business models that the company can target, explore and perhaps eventually profit from. So, while a CIO looks internally and a CTO looks externally, a CDO’s gaze is set on a more distant horizon.

Costs vs. benefits

As mentioned, these are three of the most common IT executive positions. Their specific objectives and job duties may vary depending on the business in question. And they are by no means the only examples of such positions. There are many variations, including Chief Marketing Technologist and Chief Information Security Officer.

So, getting back to our original question: is this a good time to add one or more of these execs to your staff? The answer very much depends on the financial strength and projected direction of your company. These positions will call for major expenditures in hiring, payroll and benefits. Our firm can help you weigh the costs vs. benefits.

© 2020